SAP reported better-than-expected first quarter results but the company is taking a hit on currency rates and noted geopolitical risks.

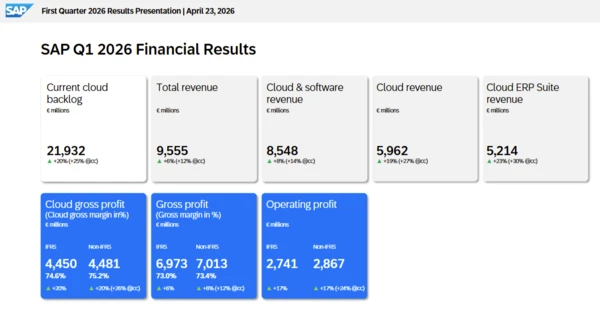

The company reported first quarter non-IFRS earnings of €1.72 a share on revenue of €9.56 billion, up 6% from a year ago. IFRS earnings in the quarter were €1.66 a share. The company’s current cloud backlog was €21.9 billion, up 20% from a year ago. In constant currency, cloud backlog was up 25%.

SAP’s currency hit was obvious in its cloud revenue. SAP’s first quarter cloud revenue was up 19% in the first quarter, but up 27% in constant currency. Cloud ERP revenue was up 23% in the first quarter, but increased 30% in constant currency. Simply put, a weaker US dollar is a big issue for SAP, which reports results in Euros.

However, SAP had a good setup into the first quarter earnings report because share sold off due to ServiceNow’s earnings report.

Christian Klein, CEO of SAP, said the company had a strong start to the year and is seeing momentum in business AI. “We are growing faster than the market and are gaining share as customers expand across our Suite and with our AI solutions. At Sapphire, we will show how we are taking the next leap forward,” said Klein.

Sapphire kicks off in Orlando, FL next month.

SAP CFO Dominik Asam said the company has “remained focused on managing our cost base and maintaining profitability as we navigate an increasingly complex and uncertain macroeconomic and geopolitical environment.”

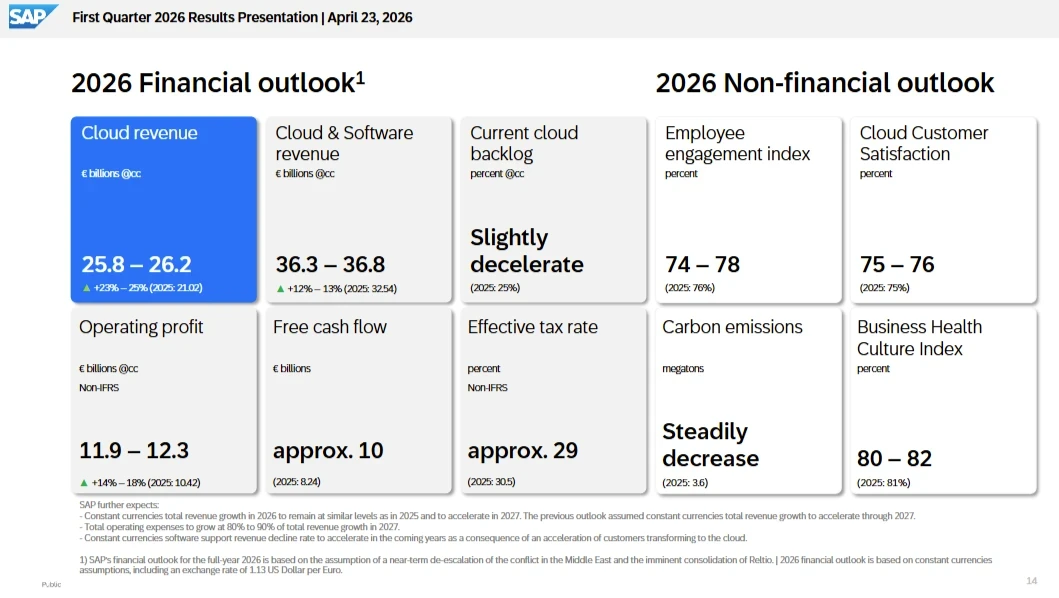

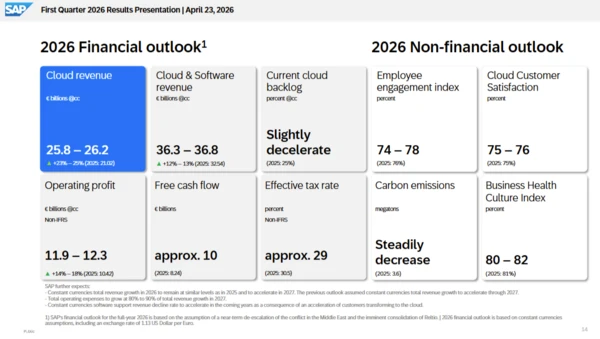

As for the outlook, SAP projected second quarter cloud revenue of €25.8 billion to €26.2 billion, up 23% to 25% from a year ago. SAP’s cloud and software revenue in the second quarter will be up 12% to 13% at constant currencies. Non-IFRS operating profit at constant currencies will be up about 14%.

SAP added that revenue growth at constant currencies in 2026 will be similar to 2025 with acceleration in 2027. SAP had projected accelerating growth through 2027.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment