Argument that the current BoJ mix is not being rewarded. Indeed, its being punished as trilemma narrative takes hold

A rift on ‘Operation Twist’ offers a strong way forward – hike policy rates while reduce the aggressive taper

Could actually be both macro supportive and market savvy

Best version of the policy relies on a degree of market surprise, with upside surprise on the policy rate

Could turn dynamics around. In Japan, higher savings rate can actually be consumer supportive

We’ll perhaps discuss this in more detail elsewhere, but its worth quickly outlining how the BoJ has a fairly compelling route to deal with its trilemma on policy, yields, and the yen: enacting an asymmetric rift on the idea of ‘Operation Twist’. Rather than selling short and buying long, this version would raise the policy rate (and more than expected) while significantly slowing its aggressive balance sheet taper. The argument is highly persuasive.

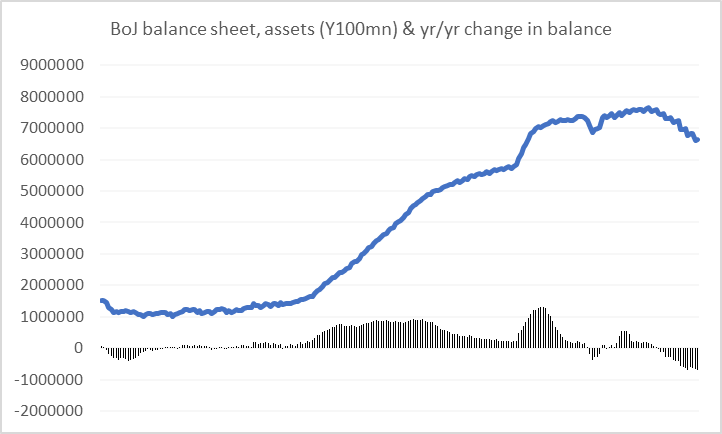

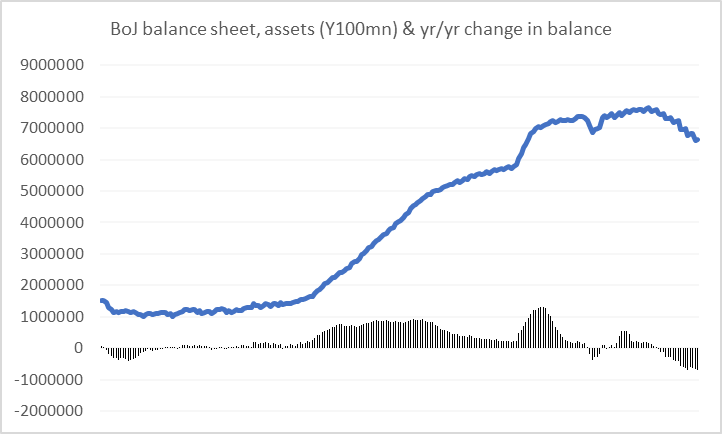

At present, the BoJ is passively tapering to the tune of 7–8% of GDP—a massive degree of quantitative tightening—while the Fed has pivoted back to low key liquidity management. Despite this, the yen is getting zero ‘credit’ from the market for its relative liquidity tightening. Instead, short-end rates, carry dynamics, and a persistent ‘policy bind’ narrative continue to fuel yen weakness. This narrative is adding to long-end yields spiking aggressively, compounding fiscal pressures and generating a vicious selling cycle.

Moving to this modified ‘Twist’ framework rebalances the BoJ’s response in a way that is macro-supportive and market-savvy. First, it bolsters credentials in the market’s eyes by backing up FX interventions with higher policy rates, effectively limiting the Fed-driven widening of overnight and short-term swap spreads. To really gain leverage, the policy rate should surprise to the market upside. Second, it directly tackles the long-end ‘doom loop’ by cushioning JGB balance (albeit at the risk of giving the government room to accommodate more fiscal spending). Furthermore, raising policy rates in Japan can be consumption-supportive—or at least neutral—given that the positive income effect for a population of savers structurally outweighs the substitution effect. Limiting yen weakness would also be net economy supportive at current levels.

There is a strong case to push this aggressive jailbreak move further by surprising the market with a 50bp (or higher) hike in June, alongside a formal slowdown of the taper. While such bold choreography is historically out of character for the Bank, it would be a well-reasoned, decisive approach and a more sedate version would be a more measured trend of upside surprise to the trajectory over coming months. Barring a maximum shock, a combined June rate hike, a tempered QT taper, and coordinated MoF interventions offer significant potential to cap (even squeeze?) the yen’s multi-month slide that has become quite stretched in terms of degree and valuations. While unlikely, the upside hike surprise could actually see quite a notable yen reaction.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment