Average long-term US mortgage rises to 6.94% after marking fourth-straight weekly increase

LOS ANGELES (AP) — The average long-term U.S. mortgage rate rose for the fourth consecutive week, another setback for prospective homebuyers just as the spring homebuying season gets going.

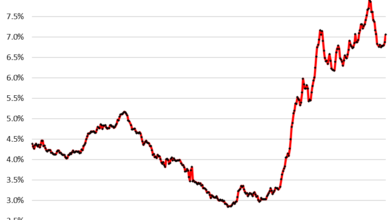

The average rate on a 30-year mortgage rose to 6.94% from 6.90% last week, mortgage buyer Freddie Mac said Thursday. A year ago, the rate averaged 6.65%. The average rate is now just below its highest level since mid-December, when it was 6.95%.

When mortgage rates rise, they can add hundreds of dollars a month in costs for borrowers, limiting how much they can afford in a market already out of reach for many Americans. They also discourage homeowners who locked in rock-bottom rates two or three years ago from selling.

Rates have been creeping higher in recent weeks as reports showing stronger-than-expected inflation at the consumer and wholesale levels and the economy stoked worries among bond investors that the Federal Reserve will wait until later this year before it begins cutting interest rates. A closely followed inflation report on Thursday showed showed prices across the country rose pretty much as expected last month.

Investors’ expectations for future inflation, global demand for U.S. Treasurys and what the Fed does with interest rates can influence rates on home loans.

Despite the recent increase, the average rate on a 30-year mortgage is still down from the 23-year high of 7.79% it reached in late October.

The pullback in rates in November and December helped lift sales of previously occupied U.S. homes by 3.1% in January versus the previous month to the strongest sales pace since August.

Still, the recent uptick in rates is an unwelcome shift for would-be homebuyers just as the spring homebuying season ramps up.

“The recent boomerang in rates has dampened already tentative homebuyer momentum as we approach the spring, a historically busy season for homebuying,” said Sam Khater, Freddie Mac’s chief economist. “While sales of newly built homes are trending in a positive direction, higher rates and elevated prices continue to pose affordability challenges that may leave potential homebuyers on the sidelines.”

Competition for relatively few homes on the market and elevated mortgage rates are limiting house hunters’ buying power on top of years of soaring prices.

Already there are signs that the rise in rates in recent weeks has had an impact on home sales.

Contract signings on U.S. homes fell 4.9% in January from the previous month and were down 8.8% from a year earlier, the National Association of Realtors said Thursday. The report is a barometer of future home purchases as there’s typically a lag of a month or two between a signed contract and a completed sale.

Meanwhile, home loan applications have declined for three consecutive weeks, according to the Mortgage Bankers Association.

Homeowners seeking to refinance got some good news this week. Borrowing costs on 15-year fixed-rate mortgages, popular with homeowners refinancing their home loans, declined this week, pulling down the average rate to 6.26% from 6.29% last week. A year ago it averaged 5.89%, Freddie Mac said.