The global payments landscape is undergoing a structural transition as onchain fiat instruments move from speculative retail instruments to institutional settlement rails. This shift is marked by two major infrastructure initiatives: the June 30, 2026, announcement

of Open USD, denoted as OUSD, a shared stablecoin network backed by a consortium of over 140 corporate signatories, and the planned launch in the first half of 2027 of a tokenized deposit network operated by The Clearing House, which is co-owned by the largest

commercial banks in the United States.

Led by Open Standard, an independent company, OUSD presents a collaborative, partner-governed model that directly challenges the traditional single-issuer structures of Tether and Circle. Led by founding Chief Executive Officer Zach Abrams, who previously

co-founded the stablecoin infrastructure provider Bridge (acquired by Stripe for 1.1 billion dollars in 2025), Open Standard aims to realign the underlying economics of the stablecoin float. This analysis evaluates the architectural design of Open USD, compares

its regulatory posture with Facebook’s defunct Libra project, assesses its competitive positioning against the USDC-USDT duopoly, and contrasts its utility against the banking sector’s emerging tokenized deposit networks.

The Genesis and Mechanics of Open USD

Open

Open

USD is engineered as shared payment infrastructure rather than a proprietary commercial product. The initial signatory roster spans payments networks including Visa, Mastercard, American Express, and Discover; financial institutions such as BNY, BlackRock,

Standard Chartered, and DBS; tech giants Google, IBM, and Samsung Electronics; and crypto platforms Coinbase, Solana, Base, and Aave. The breadth of this alliance reflects a consensus that scaling stablecoins for global workloads requires open, low-cost, and

aligned infrastructure. Stripe’s corporate leadership has indicated that OUSD will serve as the default stablecoin for businesses running on Stripe, while BNY executives project that the stablecoin market could scale to 1.5 trillion dollars by 2030.

The protocol operates on three primary operational mechanics: zero-cost transactional paths, partner-level reserve distribution, and consortium governance.

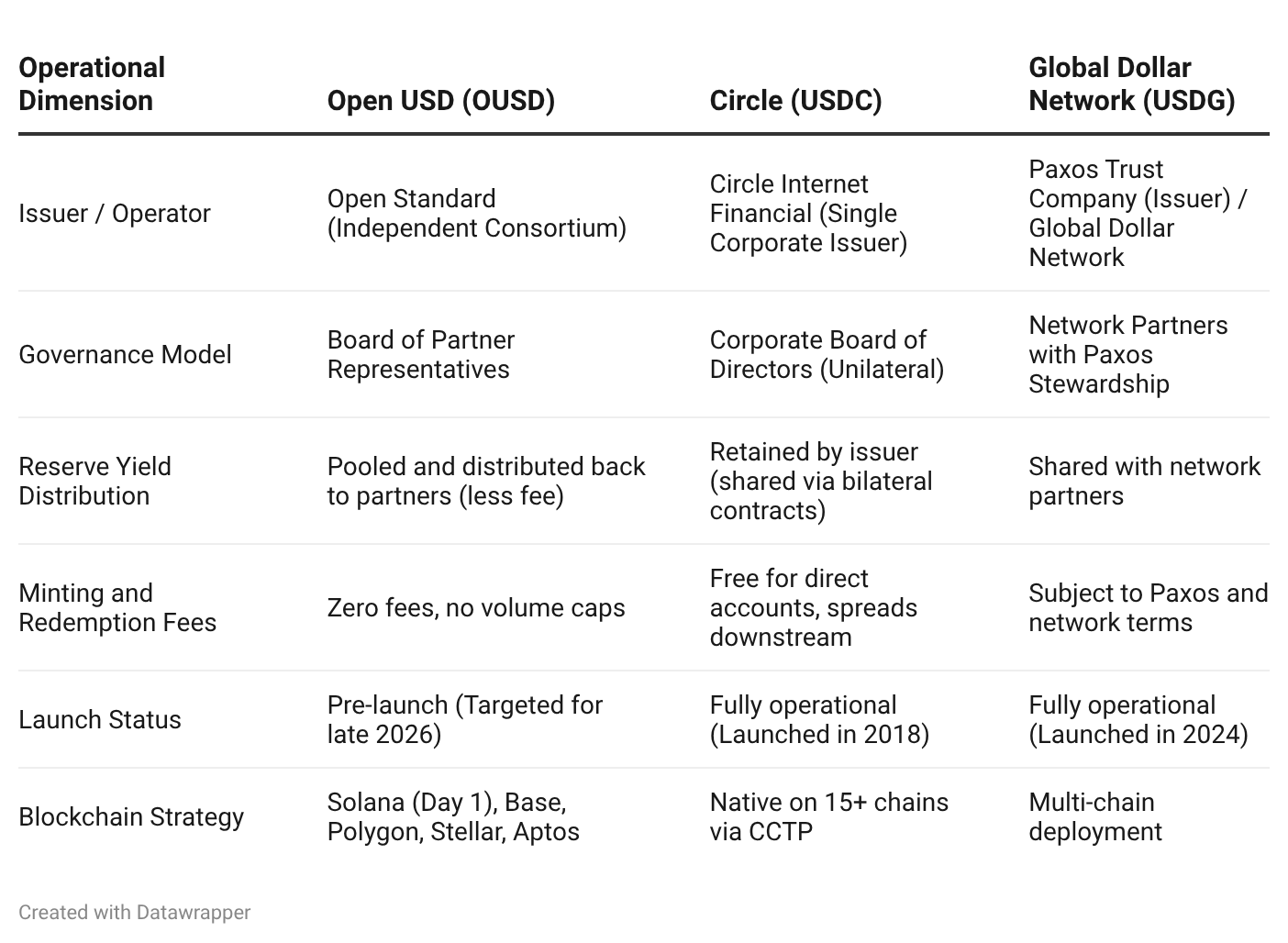

Traditional stablecoin models restrict minting and redemption to select institutional partners, often applying tiered fees, volume limits, or clearing delays through proprietary banking networks. Open USD eliminates these transaction-level costs. Under the

Open Standard model, participating businesses can deposit fiat dollars and receive OUSD tokens onchain, or redeem tokens back to physical fiat at par, with zero minting or burning fees and no artificial volume caps. By removing transaction friction, Open Standard

seeks to incentivize high-volume corporate treasury operations, merchant settlement, and cross-border routing.

The second mechanical departure is the distribution of reserve earnings. Traditional issuers manage backing assets (cash and short-duration Treasury bills) and retain 100 % of the interest income. At high interest rates, this model generates exceptional

profitability for the issuer, while the distributors and integrations that drive token adoption receive no direct financial upside.

Open USD inverts this model: all interest income generated by the underlying reserves is pooled by Open Standard. After deducting a small management fee to fund compliance, technical operations, and custody fees, the remaining yield is distributed back to

the partner network. This structure transforms onchain dollars into a productive asset for payment processors, exchanges, and merchant acquirers.

The distribution of yield to consortium partners can be represented as:

In this equation, Rpartner represents the net yield routed back to the participating partner network,

Rgross is the gross yield earned on the underlying reserve assets, and

Cmanagement is the operational cost deduction retained by Open Standard.

The third mechanic is the collaborative governance model. Open Standard operates as an independent company whose board is drawn directly from its partner base. Material decisions, such as reserve policies, custodian and auditor selection, chain expansions,

and blocklisting, are decided by a partner-led board rather than a single corporate issuer. This collaborative oversight provides the operational neutrality necessary for competing financial institutions to settle on a single shared rail.

OUSD is engineered as an onchain token. The platform will launch natively on Solana and Base, with subsequent rollouts planned for Polygon, Stellar, Aptos, and Ripple’s Tempo infrastructur. Furthermore, its integration with Aave (the largest onchain lending

market) and institutional custody networks like Fireblocks ensures immediate ecosystem utility upon deployment.

Open USD vs Tether and Circle

The

The

stablecoin market has long been dominated by the Tether (USDT) and Circle (USDC) duopoly. Tether maintains dominance in offshore transactional liquidity and retail trading pairs, while Circle’s USDC is the primary regulated settlement asset for domestic, institutional,

and decentralized finance protocols, boasting a market capitalization of approximately 73.7 billion dollars as of late June 2026.

Both Tether and Circle operate under a vertically integrated, single-issuer model. They issue the token, manage the reserve asset portfolio, and retain the entire yield generated by those reserves on their respective balance sheets.

Under this traditional model, the value created by distribution channels is entirely captured by the issuer. Payment networks like Visa and Mastercard route billions in stablecoin transactions, and fintechs like Stripe and Shopify provide the merchant interfaces,

yet they receive zero share of the reserve interest.

Open USD represents an industry-led revolt against this economic capture. Historically, cooperative consortia have emerged to break entrenched monopolies, such as the Open Handset Alliance developing Android to counter Apple, or Airbus forming to challenge

Boeing. By shifting the yield from the balance sheet of a single issuer to the profit-and-loss statements of the distribution partners, Open Standard introduces a game-theoretic incentive for major platforms to migrate their transactional volume away from

USDC and USDT.

The structural threat of this model was demonstrated on June 30, 2026, when Circle’s stock (CRCL) fell 17.55 % to a four-month low following the Open Standard announcement. This market reaction reflects the vulnerability of Circle’s margin structure, which

relies on retaining the yield on USDC’s reserves.

This competitive dynamic is further complicated by Coinbase’s involvement in the Open Standard consortium. Coinbase and Circle co-created the Centre Consortium to launch USDC, and they continue to share reserve revenue under a commercial agreement that is

reportedly up for renewal in August 2026. Circle paid Coinbase over 900 million dollars in 2024 under this arrangement to incentivize USDC distribution on the exchange.

Coinbase’s decision to join a rival consortium that shares reserve economics raises the strategic stakes. This move provides Coinbase with significant leverage in its impending negotiations with Circle, signaling that if Circle does not offer highly favorable

terms, Coinbase can leverage its retail and institutional distribution rails to route volume toward OUSD.

However, the vertically integrated models of Tether and Circle retain operational advantages over a consortium model. First, single-issuer models benefit from high decision-making velocity. Circle and Tether can unilaterally execute protocol upgrades, freeze

compromised smart contracts, expand to new public blockchains, and negotiate commercial deals without consulting a broad partner base.

Open Standard, by contrast, must govern through consensus across a board composed of 140-plus partners, many of whom are direct competitors in the traditional payment space, such as Visa and Mastercard, or Stripe and Adyen. This multi-stakeholder governance

model can introduce bureaucratic friction, slowing down technical iteration, chain expansions, and critical incident response times.

Furthermore, OUSD faces an asymmetric launch challenge. Because it is pre-launch, its claims regarding zero-cost minting and partner reserve sharing remain untested in production. Tether and USDC possess deep onchain liquidity, established secondary market

integrations, and years of audited regulatory compliance. While major exchanges like Coinbase, OKX, and Bybit are OUSD partners, these platforms will support multiple stablecoins rather than ceding their existing revenue models. For OUSD, translating corporate

signatures into active onchain transaction volume remains a significant hurdle.

Disclaimer:

Fintech Wrap Up aggregates publicly available information for informational purposes only. Portions of the content may be reproduced verbatim from the original source, and full credit is provided with a “Source: [Name]” attribution. All copyrights and

trademarks remain the property of their respective owners. Fintech Wrap Up does not guarantee the accuracy, completeness, or reliability of the aggregated content; these are the responsibility of the original source providers. Links to the original sources

may not always be included. AI is used to produce some pieces of this article. For questions or concerns, please contact us at sam.boboev@fintechwrapup.com.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment