Short-term fixed rates fall but SVRs and longer-fixed rates climb – Moneyfacts

Average two- and five-year fixed rates have fallen from their peak in September, but standard variable rates (SVRs) and 10-year fixed rates have gone up.

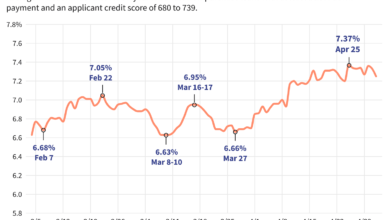

According to the latest figures from Moneyfacts, since September 2023 average two-year fixed rates have fallen from a peak of 6.7 per cent to 5.76 per cent in March.

Average five-year fixed rates have decreased from a high of 6.19 per cent in September last year to 5.34 per cent currently.

The average 10-year fixed rate stood at 5.82 per cent in September 2023, but has continued to climb over that period to 5.87 per cent in February and 5.98 per cent in March.

The average SVR has also continued to climb, coming to 5.82 per cent in September and then going up to 5.87 per cent in February and 5.96 per cent in March.

| Average mortgage rates | Sept-23 | Feb-24 | Mar-24 |

| SVR | 8.09 per cent | 8.17 per cent | 8.18 per cent |

| Two-year fixed rate mortgage | 6.7 per cent | 5.56 per cent | 5.76 per cent |

| Five-year fixed rate mortgage | 6.19 per cent | 5.18 per cent | 5.34 per cent |

| 10-year fixed rate mortgage | 5.82 per cent | 5.87 per cent | 5.98 per cent |

Source: Moneyfacts

‘Downward turn’ in fixed mortgage rates reversing

Rachel Springall, finance expert at Moneyfactscompare.co.uk, said that the “downward turn” in fixed mortgage rates has “gone in the opposite direction over the past month, with lenders vigorously repricing deals in response to volatile swap rates”.

She continued: “It is worth noting that rates are much lower than six months ago, when both the average two- and five-year fixed mortgage rates were over six per cent. The last time the Bank of England increased base rate was back in August 2023, but no change does not mean stagnation in mortgage rates as other influences remain at play, so borrowers must not be complacent if they are searching for a new deal.

“Indeed, lenders have been quick to reassess their rate pricing over the past month and even pulled deals from the market. It is vital lenders consider the volatility surrounding swap rates, so mortgage rate pricing can quickly change direction in a matter of weeks. Despite notable rate cuts made between the start of January and February, the average two- and five-year rates saw a sizeable cut.”

Springall said that borrowers concerned about securing a new deal would be “wise to seek advice from an independent broker, and any existing customers should speak to their lender immediately if they are struggling with repayments”.

She noted that those coming off a fixed rate deal could be put on an average SVR of over eight per cent, which is much higher than average fixed rates.

“A typical mortgage being charged the current average SVR of 8.18 per cent would be paying around £308 more per month, compared to a typical two-year fixed rate (5.76 per cent),” Springall noted. This calculation is based on a £200,000 mortgage over a 25-year term.

She added: “First-time buyers with limited deposits would be wise to seek advice in the first instance when looking for a mortgage, but their biggest hurdle to becoming a homeowner is finding an appropriate property while affordable housing remains in short supply.”

Anna is a reporter for Mortgage Solutions and assistant editor for Specialist Lending Solutions, both B2B sister titles of YourMoney.com. She has worked as a journalist for over four years, initially in the specialty insurance sector before moving onto mortgages.