Macquarie’s green investment valuations remain volatile, market split on their worth

Johnson, a long-term Macquarie bull, sees the opportunity in renewable investments as “massive”. He forecasts renewable infrastructure equity under management will jump from $25 billion to $4 trillion by 2050, assuming a 10 per cent market share. Any slump in asset prices and realisations simply pushes out the performance fees, he says.

Increasingly, however, critics are questioning why the market isn’t scrutinising the green portfolio more closely, or at least asking how exactly Macquarie values its investments.

Investments repriced

Most of Macquarie’s investments are held off its balance sheet, in its asset management division, after the group moved them from Macquarie Capital in 2022.

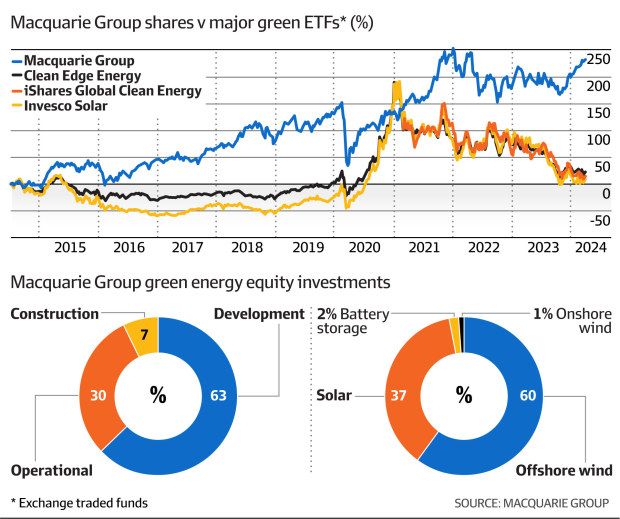

Globally, investments in renewables have been hurt by the higher interest rate environment lowering valuations, rising construction costs and the higher cost of debt. That has led to investments being repriced across the market, including the recent slump in the prices of clean energy exchange traded funds.

Unnerving these investors even more are reports that Macquarie has been slow to write down the valuations of others holding and causing tension with joint investors, including an Indian edtech investment, Byju’s.

Many investments in green infrastructure have also been accelerated because of government subsidies. Macquarie Asset Management has pushed more deeply into the United States to take advantage of the Inflation Reduction Act, which Donald Trump has said he will gut if he wins the presidency.

One of the more recent asset purchases in the group’s GIG Energy Transition Fund that a change of US government could hit is its $US325 million ($493 million) investment in Atlas Agro Holding, which it bought late last year. But realistically, it’s not held on balance sheet, and nor is it meaningful to the group.

Tiny part of holdings

More broadly, these concerns aren’t affecting investors looking to put money with Macquarie, though the issue – as it is across the sector – remains realising assets. The group closed its Macquarie European Infrastructure Fund 7 fundraising in January at a record €8 billion ($13.2 billion).

Leithner & Co’s Chris Leithner has called for the group to divest its green energy assets, questioning whether the returns will ever come through. He also points out that perhaps the reason Macquarie isn’t being hurt by these green asset issues is that they remain a tiny part of the group’s overall holdings.

Using numbers from the September 6 presentation, Macquarie “invested, committed or arranged” $2.2 billion of “green energy assets” in the last financial year. That is equivalent to 0.25 per cent of its $870.8 billion on total assets under managment, and 2.8 per cent of the increased assets under management of $75.2 billion over that 12 months.

So, despite the potential growth, the asset base remains small. For a diversified asset manager like Macquarie, with a successful track record, pushing out sales ahead of a better environment isn’t a major issue.

But some say that may not come. Leithner is questioning the merit of investing in green assets, arguing that the investment case for green energy investments has not been proved.

He compares the performance of investing $100 in the S&P 500 against the Global Clean Energy Index, which consists of global solar and wind companies (including troubled Danish wind giant Orsted).

Since July 2008, an investment of $100 in the S&P 500 has grown to $401 – a compound annual growth rate of 9.4 per cent a year for 15 years. In contrast, the clean energy index over the year to April 5 has fallen 30.5 per cent. Since 2008, the investment of $100 has shrunk to just $39 – that’s compound growth of negative 5.9 per cent a year and total underperformance of 15.3 per cent a year for 16 years.

For many, the combination of Macquarie’s track record of identifying long-term trends and the small exposure to the green energy sector means that can be pushed to one side.

Those bullish on Macquarie, including MST’s Johnson, note shares have underperformed global specialist asset manager peers who rallied before expected interest rate falls.

And there are signs that Macquarie agrees trading assets may be getting easier. It has mandated advisers to sell data centre group AirTrunk, where earnings have increased seven times since Macquarie invested. On paper, AirTrunk looks like it could be worth $13 billion to $14 billion (including $6 billion in debt), according to those taking a look.

For most investors, there’s been little upside in betting against Macquarie, particularly when financial markets are in full gear. And, as one investor points out, Macquarie is betting on itself, buying back shares on market.

“They’re one of the shrewdest users of capital, they raise at the top. For them to be buying back now, they must know something we don’t,” that investor says.

Source link