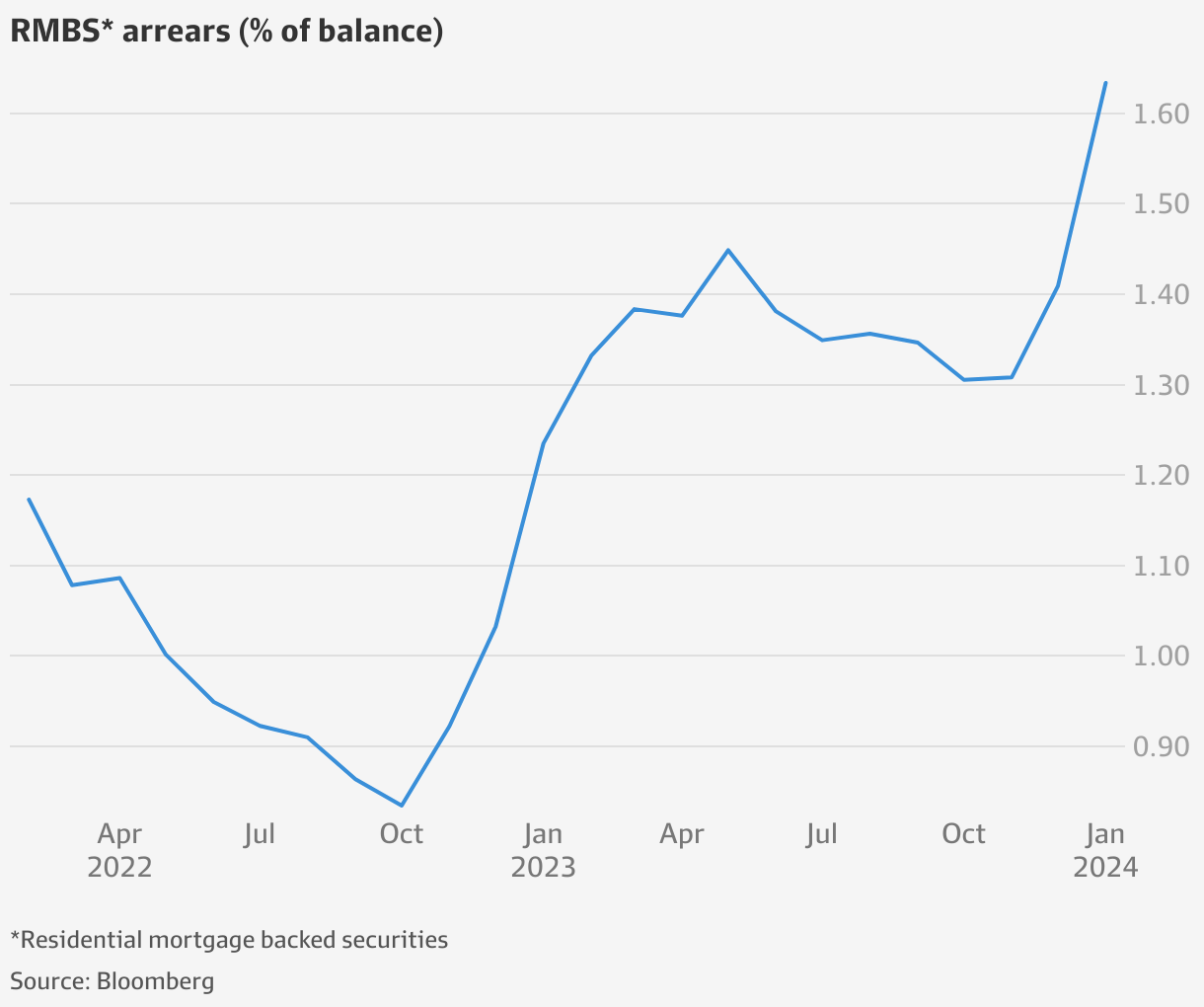

Mortgage stress rates hit fastest pace in at least two years

“Inflation may be a little bit more resilient than the market is expecting, so I don’t see rate cuts coming this year,” Mr Austin said, adding that, despite the increase, arrears were very low base. The effects were starting to be felt at major lenders, he said.

National Australia Bank, for example, said credit impairment costs rose 17 per cent to $193 million in September-December from the preceding three months.

Westpac announced a $189 million impairment charge for the first quarter that was 47 per cent higher than the second half average. Ninety-day arrears – the most at risk of defaulting – rose 9 basis points to 0.95 per cent at Westpac in the December quarter. At NAB, the number was steady at 0.75 per cent of its home lending book.

“The last leg of this tightening cycle could prove to be the most challenging, as savings are depleted, unemployment rises, and higher interest rates continue,” S&P warned earlier this week.

The RBA has held rates at 4.35 per cent since its last quarter-percentage point rise in November, which marked the 13th increase since it began tightening monetary policy in May 2022.

Firstmac’s James Austin said that, despite arrears rising, they were coming off a very low base. Jamila Toderas

“Mortgage books across the country have been pretty resilient, and It has probably surprised many,” Mr Austin said. “But there will be further deterioration to come.”

Incoming National Australia Bank boss Andrew Irvine said on Friday that “inflation is not dead yet”.

“Inflation is awful. You only have to talk to consumers who are struggling with the price of fuel, the price of groceries, and it’s in everybody’s interest to get inflation under control,” Mr Irvine told ABC Radio.

“I am optimistic that we’re moving in that direction. I think overnight in the US we had a really good inflation print. Hopefully, we see some of that come in Australia, and I think that will give the RBA the ability to look at interest rates and start to bring them down when they’re comfortable,” he said.

Ross McEwan, Mr Irvine’s predecessor at NAB, said inflation would stay above 3 per cent until the end of the year. “We’re still not predicting interest rates coming down until the final quarter of this calendar year,” Mr McEwan said.

“You get tax cuts coming through in July, which will be helpful, and then interest rates starting to drop off in the latter part of this year and not before. Inflation has to be crushed,” he said, adding most NAB customers were still “in good shape”.

Investors outperform at-risk owner-occupiers

According to datasets published by Bloomberg, close to 1.9 per cent of owner-occupiers are delinquent on their home loan compared to 1.3 per cent for investors.

Mr Austin said this was a sustained trend over time, which had sparked Firstmac to start allocating more investor loans into its residential mortgage-backed securities issues.

The Brisbane-based lender last week priced a record $2 billion deal – nearly half of the underlying collateral was investor loans, compared with the more typical rate of about a third.

Mr Austin said, while it was initially a hard sell to international investors who typically assume investor loans will perform worse than owner-occupiers, there was overwhelming demand once they realised the trend was reversed in Australia.

He said this was because of the “non-recourse” mortgage system in the US, where borrowers can strategically default on a loan, even if they can service the debt, and walk away from the property without repercussions from the lender. In Australia, the system is “recourse” so lenders can pursue borrowers for their other assets if they were to default on their home loan.

Strategic defaults are more common with investor loans in the United States, Mr Austin said, whereas in Australia if “you default on one loan, you default on the other”.

“There’s always a view that investor loans are somehow riskier than owner-occupier,” he said. “Investment loans typically always perform better, and that flies in the face of what the regulators and rating agencies say. They take their lead from offshore – in both cases it is a typically US-centric view.”

He described rules that require lenders to hold more capital against investor loans as a “hangover” from the bursting of the US real estate bubble during the GFC in 2008, arguing that regulators and rating agencies should tailor their approach more to the local trend.

Mr Austin said the “US-centric” view had heightened cost of living issues.

“There is greater capital that is being applied to investor loans, which means the rates being charged to investor loans are higher, and that means that the people who are renting are paying higher rent,” he said.

Source link