Asian Stocks Fall Amid War Tensions, Metals Rally: Markets Wrap

(Bloomberg) — Shares in Asia slipped to a six week-low as traders grappled with tensions in the Middle East, disappointing bank earnings and the prospect of the Federal Reserve keeping interest rates higher for longer.

Most Read from Bloomberg

A gauge for the region’s equities fell, tracking Friday’s drop in US stocks. Benchmarks in Hong Kong, Japan and South Korea all declined while shares in mainland China rose, led by the energy sector. Futures for US equities edged higher in Asian trading after the S&P 500 suffered its worst session since January on Friday amid a flight to safety.

But global markets showed signs of stability even after unprecedented attack on Israel at the weekend. Iran said “the matter can be deemed concluded,” and President Joe Biden reportedly told Israeli Prime Minister Benjamin Netanyahu that the US won’t support an Israeli counterattack against Iran.

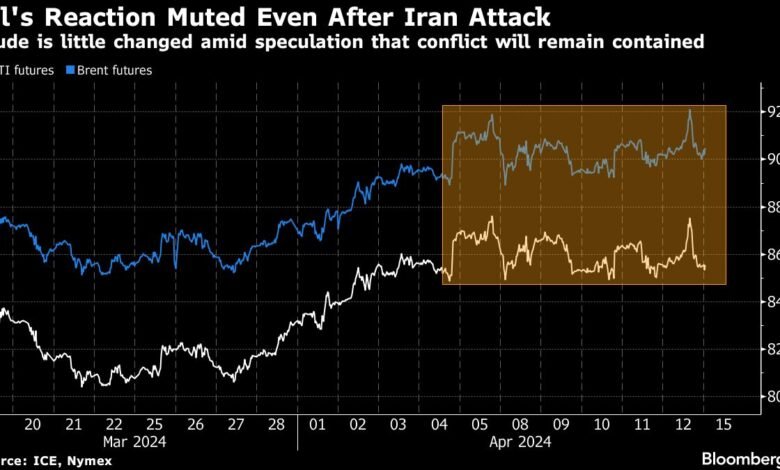

Oil shrugged off the attacks, with prices easing on speculation that the conflict would remain contained as global benchmark Brent crude steadied to around $90 a barrel. Meanwhile, aluminum and nickel surged following new US and UK sanctions that banned deliveries of any Russian supplies after midnight on Friday.

“Geopolitical risks are back on the radar with Iran’s missile and drone attack on Israel,” said Redmond Wong, a market strategist at Saxo Capital Markets. “While market response was subdued in early Asia, volatility and nervousness is likely with eyes on any further headlines coming out of the Middle East.”

Most Group-of-10 currencies strengthened against the greenback Monday while Treasuries were little changed in Asia after yields slipped in the previous session.

Meanwhile, Chinese authorities held a key interest rate unchanged while withdrawing cash from the banking system for a second consecutive month. The operation came even after price growth stalled last month, fueling calls for more stimulus.

Elsewhere, developer China Vanke Co. said it’s making plans to resolve liquidity pressure and short-term operational difficulties as China’s top leaders have grown increasingly alarmed about the country’s protracted real estate crisis and its effect on the sluggish economy.

With investors already rattled by sticky inflation and the prospect of higher-for-longer interest rates, the escalation of the Middle East crisis may inject fresh volatility into markets. As the conflict widens, many say oil could surpass $100 a barrel and expect a flight to Treasuries, gold and the dollar, along with further stock-market losses.

Bitcoin rallied after it sank almost 9% in the wake of the attacks. Stock markets in Saudi Arabia and Qatar posted modest losses under thin trading volumes on Sunday. Israel’s equity benchmark fluctuated between gains and losses at least nine times before closing with a small gain.

As Wall Street’s earnings season kicked off, big banks’ results offered the latest window into how the US economy is faring amid an interest-rate trajectory muddied by persistent inflation.

JPMorgan Chase & Co. and Wells Fargo & Co. both reported net interest income — the earnings they generate from lending — that missed estimates amid increasing funding costs. Citigroup Inc.’s profit topped analysts’ estimates as corporations tapped markets for financing and consumers leaned on credit cards — signs that a prolonged period of elevated interest rates will benefit big banks.

“Many economic indicators continue to be favorable. However, looking ahead, we remain alert to a number of significant uncertain forces,” JPMorgan’s Chief Executive Officer Jamie Dimon said. He cited the wars, growing geopolitical tensions, persistent inflationary pressures and the effects of quantitative tightening.

Traders will soon shift to looming economic data as they refine bets on central bank easing cycles, as well as the International Monetary Fund and World Bank spring meetings in Washington. This week, Chinese growth data and Japan, Eurozone and UK inflation readings are due.

Key events this week:

-

Eurozone industrial production, Monday

-

US retail sales, empire manufacturing, business inventories, Monday

-

Federal income taxes due in the US, Monday

-

IMF and World Bank spring meetings start in Washington, Monday. The main ministerial meetings will be held April 17-19

-

Canada CPI, Tuesday

-

China property prices, retail sales, industrial production, GDP, Tuesday

-

UK jobless claims, unemployment, Tuesday

-

New Zealand home sales, CPI, Wednesday

-

Eurozone CPI, Wednesday

-

UK CPI, Wednesday

-

Australia unemployment, Thursday

-

Japan CPI, Friday

-

India’s elections begin, Friday

Some of the main moves in markets:

Stocks

-

S&P 500 futures rose 0.2% as of 10:51 a.m. Tokyo time

-

Nikkei 225 futures (OSE) fell 1.1%

-

Japan’s Topix fell 0.6%

-

Australia’s S&P/ASX 200 fell 0.6%

-

Hong Kong’s Hang Seng fell 1.3%

-

The Shanghai Composite fell 0.2%

-

Euro Stoxx 50 futures were little changed

Currencies

-

The Bloomberg Dollar Spot Index was little changed

-

The euro was little changed at $1.0648

-

The Japanese yen fell 0.2% to 153.56 per dollar

-

The offshore yuan was little changed at 7.2612 per dollar

-

The Australian dollar rose 0.1% to $0.6475

Cryptocurrencies

-

Bitcoin rose 2.3% to $65,322.76

-

Ether rose 2% to $3,130.31

Bonds

-

The yield on 10-year Treasuries was little changed at 4.53%

-

Japan’s 10-year yield declined one basis point to 0.840%

-

Australia’s 10-year yield declined four basis points to 4.22%

Commodities

-

West Texas Intermediate crude fell 0.3% to $85.41 a barrel

-

Spot gold rose 0.4% to $2,354.29 an ounce

This story was produced with the assistance of Bloomberg Automation.

–With assistance from Yongchang Chin.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.

Source link