The macroeconomic environment today presents compelling evidence of why fiat currency fails and gold endures through systematic monetary debasement and fiscal pressures. Modern economic systems face unprecedented challenges as traditional fiscal constraints dissolve under the weight of mounting government obligations and demographic pressures. The mathematical impossibility of servicing exponential debt growth through conventional means has pushed monetary authorities into uncharted territory, where currency debasement becomes not merely a policy option but an apparent necessity.

What Are the Fundamental Economic Forces Behind Currency Debasement?

The Debt-to-GDP Spiral That Destroys Purchasing Power

Global debt dynamics have entered dangerous territory across developed economies. Advanced nations now carry debt burdens that mathematically cannot be serviced through taxation alone without triggering economic collapse. Japan exemplifies this trajectory, with government debt reaching approximately 264% of GDP as of 2024, according to the Ministry of Finance Japan’s fiscal statistics.

The mechanics are straightforward yet politically intractable. When debt service costs exceed reasonable taxation capacity, governments face three stark choices. They can implement severe austerity measures, dramatically increase tax rates, or inflate the debt burden away through monetary expansion.

Historical evidence consistently demonstrates that political systems choose the third option. Austerity proves politically toxic, while meaningful tax increases face similar resistance. Monetary expansion appears initially painless, transferring costs to future periods while providing immediate fiscal relief.

Furthermore, understanding these dynamics reveals precisely why fiat currency fails and gold endures across different monetary regimes. The political constraints that prevent fiscal responsibility create predictable patterns of currency debasement, making hard assets increasingly attractive to preservationists of wealth.

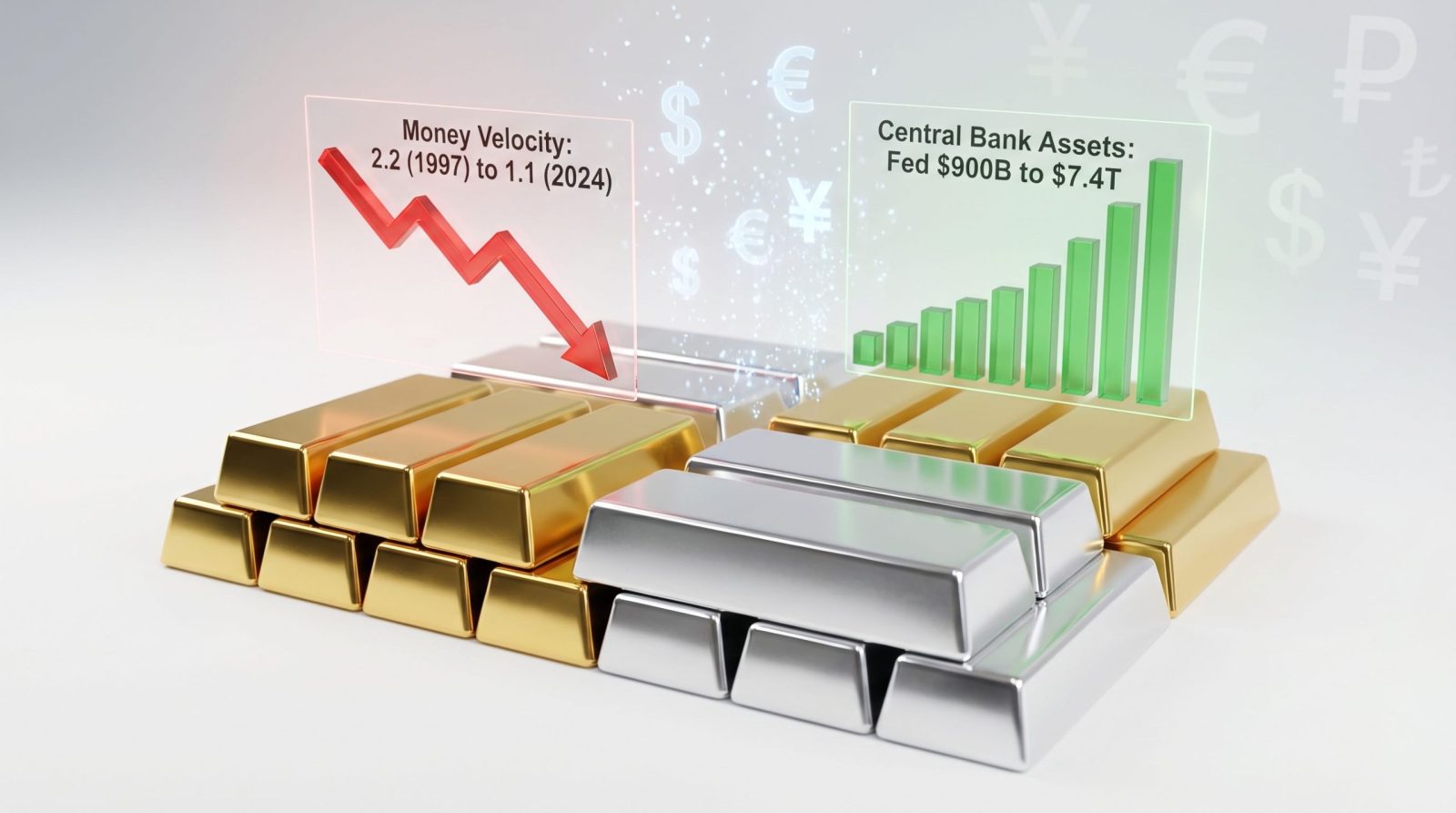

Central Bank Balance Sheet Expansion Since 2008

The scale of monetary accommodation since the 2008 financial crisis represents an unprecedented experiment in economic history. Central bank asset purchases have fundamentally altered the relationship between monetary policy and fiscal financing.

Federal Reserve Expansion:

- 2008 Assets: $900 billion

- 2024 Assets: $7.25 trillion

- Expansion Multiple: 8.1x

European Central Bank Growth:

- 2008 Assets: €940 billion

- 2024 Assets: €8.2 trillion

- Expansion Multiple: 8.7x

Bank of Japan Trajectory:

- 2008 Assets: ¥94 trillion

- 2024 Assets: ¥731 trillion

- Expansion Multiple: 7.8x

These figures reflect a fundamental shift from traditional central banking toward direct fiscal accommodation. When monetary authorities purchase government securities on this scale, they effectively finance spending through currency creation rather than private sector savings.

The Cantillon Effect and Wealth Transfer Mechanisms

Currency creation creates systematic wealth redistribution through what economists term the Cantillon Effect. This process describes how newly created money benefits initial recipients while imposing costs on subsequent holders through delayed price increases.

Financial institutions receive newly created liquidity first, directing this capital toward asset markets before it reaches the broader economy. Consequently, asset prices inflate faster than wages or consumer goods, creating divergent inflation patterns. These developments support the broader gold surge explained by current monetary conditions.

Asset Price Inflation vs. Consumer Prices:

- Median U.S. home prices: +105% (2008-2024)

- Median nominal wages: +65% (same period)

- Purchasing power gap: 40 percentage points

This mechanism systematically transfers wealth from wage earners and savers toward asset holders. Real estate and equity markets experience artificial demand as investors seek inflation hedges, further concentrating wealth among those holding financial assets rather than earning income through labor.

When big ASX news breaks, our subscribers know first

How Do Modern Monetary Systems Differ From Historical Sound Money Principles?

The Bretton Woods Collapse and Its Long-Term Consequences

The termination of dollar-gold convertibility on August 15, 1971, represents the most significant monetary regime change in modern history. Under the Bretton Woods system, foreign governments could exchange dollars for gold at $35 per troy ounce, providing a natural constraint on U.S. monetary expansion.

When President Nixon suspended this convertibility, global monetary systems lost their anchor to physical commodities. This change eliminated the primary mechanism that historically restrained government spending and monetary creation.

Trade Balance Deterioration:

- U.S. trade deficit (1971): -$3.1 billion

- U.S. trade deficit (2024): -$729 billion

- Real purchasing power decline: 95% over 53 years

The absence of convertibility constraints enabled persistent trade deficits without automatic correction mechanisms. Countries could accumulate dollar reserves indefinitely without demanding gold redemption, allowing the U.S. to finance consumption through currency creation rather than production.

Velocity of Money Decline in Advanced Economies

Money velocity measures how frequently currency units circulate through the economy. Declining velocity indicates reduced economic efficiency and suggests monetary system dysfunction.

Money velocity in the U.S. has declined from approximately 2.1 in 1997 to roughly 1.5 in 2024, indicating that each dollar circulates 30% less frequently than during the late 1990s—a sign of monetary system stress and increased hoarding behaviour.

This decline reflects several concerning trends:

- Increased precautionary money holdings as confidence erodes

- Reduced business investment velocity due to uncertainty

- Asset market speculation replacing productive economic activity

- Credit market dysfunction limiting money circulation efficiency

The Brookings Institution’s research on velocity decline links this phenomenon to structural changes in how monetary policy transmits through the economy, with traditional channels becoming less effective over time.

Real Interest Rate Suppression and Capital Misallocation

Extended periods of negative real interest rates fundamentally distort economic calculation and resource allocation. When borrowing costs fall below inflation rates, profitable projects become indistinguishable from unprofitable ones, leading to systematic capital misallocation.

Historical Real Rate Periods:

- 2008-2021: Most developed economies maintained negative real rates

- 2022-2024: Real rates turned positive amid inflation surge

- Current environment: Mixed real rate regime with policy uncertainty

The Bank for International Settlements documented how negative real rates enable “zombie companies” to survive despite negative productivity. These firms consume capital without generating economic value, reducing overall productivity growth.

Zombie Firm Characteristics:

- Interest coverage ratios below 1.0 for multiple years

- Survival dependent on credit market accommodation

- Market share maintenance through below-cost pricing

- Resource consumption without value creation

What Historical Patterns Reveal About Currency Collapse Cycles?

The Weimar Republic Hyperinflation Model (1921-1923)

The German hyperinflation remains the most studied currency collapse in modern history, providing a precise template for understanding how fiscal pressures trigger monetary destruction.

Initial Conditions:

- War reparations of 132 billion gold marks imposed by Versailles Treaty

- Political impossibility of sufficient tax increases

- Democratic government instability preventing austerity implementation

Acceleration Timeline:

- July 1914: 4.19 marks per dollar (pre-war baseline)

- November 1923: 4.2 trillion marks per dollar at peak hyperinflation

- Total devaluation: 99.999999% loss of purchasing power

The critical insight involves understanding that hyperinflation results from political constraints rather than economic ignorance. The Weimar government understood monetary consequences but faced political impossibility of alternative solutions.

Modern Emerging Market Currency Crises

Contemporary currency crises follow similar patterns, though developing across different timeframes and triggering mechanisms.

Turkey Crisis (2018-2021):

- Initial trigger: Political interference with central bank independence

- Exchange rate deterioration: 3.77 TRY/USD to 16.36 TRY/USD

- Total devaluation: 77% loss of dollar purchasing power

- Contributing factors: Current account deficit, political monetary policy

Argentina’s Recurring Crises:

- Frequency: Multiple currency devaluations since 1975

- Current status: Peso has lost 99.5% of its 1975 purchasing power

- Pattern: Fiscal deficits leading to monetary accommodation and currency collapse

- Recent developments: 2023-2024 crisis requiring IMF intervention

Zimbabwe’s Complete Collapse:

- Timeline: 2000-2008 hyperinflation period

- Peak rates: Monthly inflation exceeding 231,000,000%

- Resolution: Abandonment of domestic currency entirely

- Current status: Multi-currency regime using foreign money

These examples illustrate the broader context discussed in analyses of US economy inflation debt pressures affecting developed nations.

Advanced Economy Warning Signals

Developed nations display early-stage characteristics similar to emerging market pre-crisis conditions:

Fiscal Stress Indicators:

- Government spending exceeding 40% of GDP across major economies

- Debt service costs approaching 15-20% of government revenues

- Demographic pressures requiring increased social spending

- Political constraints preventing meaningful fiscal adjustment

Central Bank Independence Erosion:

- Political pressure for accommodative monetary policy

- Yield curve control implementation (Japan, Australia experimentation)

- Direct fiscal financing through asset purchase programs

- Public criticism of monetary policy tightening attempts

Why Do Gold and Silver Maintain Purchasing Power Across Monetary Regimes?

Stock-to-Flow Ratios and Supply Constraints

Physical scarcity provides the fundamental property distinguishing precious metals from fiat currencies. Annual production represents a small fraction of existing above-ground stock, creating supply inelasticity impossible to replicate with paper money.

Annual Production vs. Existing Stock:

| Metal | Annual Mine Supply | Above-Ground Stock | Stock-to-Flow Ratio |

|---|---|---|---|

| Gold | 3,300 tonnes | 208,000 tonnes | 63 years |

| Silver | 26,000 tonnes | 1.74M tonnes | 67 years |

| Copper | 22M tonnes | 800M tonnes | 36 years |

These ratios demonstrate why precious metals resist rapid supply increases. Even dramatic price rises cannot significantly increase annual production relative to existing stocks, unlike currencies that can be created without physical constraints.

Mining Production Constraints:

- Exploration timelines: 7-15 years from discovery to production

- Capital requirements: Billion-dollar investments for major deposits

- Geological limitations: Finite high-grade ore body availability

- Environmental regulations: Increasing restrictions on new mine development

Cross-Civilization Monetary Recognition

Archaeological evidence reveals precious metals served monetary functions across isolated civilisations without cultural exchange, suggesting inherent properties rather than arbitrary convention.

Historical Monetary Adoption:

- Ancient Egypt: Gold and silver standards dating to 3000 BCE

- Classical Greece: Electrum and silver coinage systems

- Roman Empire: Bimetallic standard with gold and silver

- Chinese dynasties: Precious metal standards across millennia

- Pre-Columbian Americas: Gold and silver ceremonial and exchange use

Modern central bank behaviour reinforces this historical pattern. Despite operating fiat currency systems, monetary authorities continue accumulating gold reserves, particularly during periods of geopolitical stress.

Central Bank Gold Purchases (2018-2024):

- Annual average: Over 1,000 tonnes purchased by official sector

- Primary buyers: Emerging market central banks

- Motivation: Reserve diversification away from dollar dependence

- Trend acceleration: Increased purchases during sanctions and trade tensions

Industrial Demand Floor for Silver

Silver possesses unique industrial applications creating inelastic demand that provides a fundamental value floor independent of monetary considerations.

Industrial Consumption Breakdown:

- Solar panel manufacturing: 20% of annual silver production

- Electronics sector: 320 million ounces annually

- Medical applications: Antimicrobial properties creating growing demand

- Water purification: Industrial and municipal treatment systems

This industrial demand cannot be easily substituted, creating baseline consumption that persists regardless of investment demand fluctuations. Unlike gold, which primarily serves monetary and jewellery functions, silver’s industrial applications provide additional demand support.

Stagflation Periods and Real Asset Outperformance

Historical analysis reveals precious metals deliver exceptional returns during periods combining economic stagnation with currency debasement—precisely the conditions emerging in contemporary economies.

Historical Stagflation Performance:

- 1970s decade: Gold +2,300%, Silver +2,400%

- 2000-2011: Gold +650% during financial crisis and quantitative easing

- 2019-2024: Gold +85% amid pandemic monetary expansion

The 1970s provide the most relevant template for understanding precious metals behaviour during monetary chaos. Multiple shocks combined to create ideal conditions for hard asset outperformance. Current conditions show similar characteristics to those detailed in gold price forecast analyses.

1970s Catalysts:

- Nixon Shock (1971): End of dollar-gold convertibility

- Oil price shocks: Energy costs quadrupling twice during decade

- Persistent inflation: Consumer prices rising throughout period

- Currency instability: Multiple devaluation cycles across major economies

Currency Debasement Acceleration Indicators

Quantitative analysis reveals specific thresholds where precious metals historically outperform financial assets by dramatic margins.

When M2 money supply growth exceeds nominal GDP growth by more than 5% annually for three consecutive years, precious metals historically outperform financial assets by 200-400%.

Current Money Growth Metrics:

- U.S. M2 growth (2020-2024): Average 12% annually

- Nominal GDP growth (same period): Average 6% annually

- Excess liquidity creation: 6 percentage points above economic growth

- Duration: Four consecutive years exceeding threshold

This excess liquidity seeks inflation hedges, flowing disproportionately toward assets with supply constraints. Real estate, commodities, and precious metals benefit while fixed-income investments suffer negative real returns.

Central Bank Gold Accumulation Trends

Official sector gold purchases provide crucial insight into institutional monetary thinking. Central banks possess superior information about currency system stability and adjust reserves accordingly.

Recent Accumulation Patterns:

- 2018-2024 purchases: Over 7,000 tonnes acquired by central banks

- Primary buyers: China, Russia, Turkey, India, Poland

- Motivation shift: From dollar complement to dollar alternative

- Storage changes: Repatriation of gold from Western custody

The geographic distribution reveals emerging economies seeking independence from dollar-based monetary system. These nations possess direct experience with currency instability and recognise precious metals’ role in monetary security.

What Are the Portfolio Construction Implications for Wealth Preservation?

Allocation Frameworks During Monetary Instability

Strategic asset allocation must acknowledge different risk environments requiring distinct precious metals exposure levels. In addition, understanding why fiat currency fails and gold endures provides essential context for allocation decisions.

Risk-Adjusted Allocation Models:

| Risk Environment | Precious Metals Allocation | Rationale |

|---|---|---|

| Conservative | 5-10% | Portfolio stabilisation during normal conditions |

| Moderate Stress | 15-25% | Inflation hedge during monetary expansion |

| Crisis Environment | 30-40% | Capital preservation during currency instability |

Historical backtesting suggests optimal allocation ranges shift based on monetary policy regime rather than traditional business cycle considerations. During periods of negative real interest rates and quantitative easing, higher allocations historically provided superior risk-adjusted returns.

Implementation Considerations:

- Gradual accumulation: Dollar-cost averaging reduces timing risk

- Rebalancing discipline: Maintaining target allocations through cycles

- Tax efficiency: Understanding precious metals tax treatment

- Liquidity planning: Ensuring adequate liquid reserves for expenses

Physical vs. Paper Precious Metals Exposure

The choice between physical metal ownership and financial instruments carries significant implications during systemic financial stress.

Physical Ownership Advantages:

- No counterparty risk: Value independent of financial institution solvency

- Crisis liquidity: Tradeable during financial system disruption

- Privacy benefits: Transactions outside electronic monitoring systems

- Inflation protection: Direct hedge against currency purchasing power loss

Physical Ownership Challenges:

- Storage costs: Insurance and security expenses

- Liquidity constraints: Transaction friction compared to ETFs

- Authentication requirements: Verification needed for transactions

- Geographic concentration: Regulatory seizure risk in single jurisdiction

Paper Precious Metals Instruments:

- ETF convenience: High liquidity and low transaction costs

- Professional storage: Institutional-grade security systems

- Fractional ownership: Access without large capital requirements

- Counterparty dependency: Performance relies on financial system stability

Geographic and Political Risk Diversification

Modern portfolio theory requires extending beyond traditional asset class diversification to include geographic and political risk management.

Multi-Jurisdiction Storage Strategies:

- Domestic allocation: 40-60% in home country jurisdiction

- Foreign allocation: 40-60% in politically stable foreign jurisdictions

- Selection criteria: Rule of law, property rights protection, political stability

- Popular jurisdictions: Switzerland, Singapore, Hong Kong, New Zealand

Currency Diversification Beyond Fiat:

- Multiple currency exposure: Reducing single-currency concentration

- Real asset hedging: Precious metals as currency-independent store of value

- Correlation analysis: Understanding precious metals correlation with various currencies

- Rebalancing mechanisms: Maintaining target allocations across currency movements

The next major ASX story will hit our subscribers first

What Forward-Looking Indicators Suggest About Monetary System Stability?

Demographic Pressures on Government Finances

Population aging creates structural fiscal pressures that cannot be resolved through traditional economic growth or productivity improvements.

Demographic Trajectory Analysis:

- Worker-to-retiree ratios: Declining from 4:1 to 2:1 across developed economies

- Healthcare cost escalation: Rising faster than general inflation rates

- Pension obligations: Underfunded by estimated $200+ trillion globally

- Political constraints: Democratic systems preventing adequate reform

These pressures create mathematical certainty that government spending will rise faster than revenue capacity, forcing increased reliance on monetary financing. Unlike cyclical fiscal deficits, demographic-driven spending cannot be reduced without fundamental social contract changes.

Unfunded Liability Estimates by Country:

- United States: $159 trillion (Social Security and Medicare)

- European Union: €75 trillion across member nations

- Japan: ¥1,100 trillion in pension and healthcare obligations

- Global total: Exceeding $200 trillion in present value terms

Digital Currency Implementation and Control Mechanisms

Central Bank Digital Currencies (CBDCs) represent fundamental changes to monetary system architecture, potentially enabling direct government control over individual transactions.

CBDC Development Status:

- Pilot programs: Over 80 countries exploring CBDC implementation

- Advanced development: China, European Union, United Kingdom leading

- U.S. position: Federal Reserve research with political resistance

- Timeline projections: Widespread implementation within 5-10 years

Programmable Money Capabilities:

- Spending restrictions: Government ability to limit purchase categories

- Expiration dates: Currency losing value if not spent within timeframes

- Geographic constraints: Money functional only in specific locations

- Real-time monitoring: Complete transaction surveillance capability

These capabilities fundamentally alter the relationship between individuals and monetary authorities, potentially eliminating financial privacy and enabling direct economic control mechanisms previously impossible.

Geopolitical Fragmentation of Monetary Systems

International monetary system fragmentation accelerates as nations seek independence from dollar-based settlement systems.

Alternative Payment System Development:

- BRICS payment mechanism: Russia, China, India, Brazil collaboration

- Bilateral settlement agreements: Direct currency exchanges bypassing dollars

- Gold-backed trade proposals: Discussions of commodity-based settlement

- SWIFT alternatives: Independent financial messaging systems

Trade Settlement Evolution:

- China-Russia transactions: Increasing yuan and ruble settlement

- India-Iran oil trade: Rupee payment mechanisms

- Saudi Arabia discussions: Considering yuan for oil sales

- European independence efforts: Euro-based energy transaction systems

This fragmentation reduces global demand for dollar reserves, potentially triggering significant adjustments in U.S. monetary conditions and precious metals demand. Current developments align with analyses showing record-highs inflation hedge properties of precious metals during monetary transitions.

What Triggers the Final Phase of Currency Collapse?

The terminal phase typically begins when foreign confidence collapses before domestic rejection occurs. International investors and central banks stop accepting the currency at any reasonable exchange rate, forcing domestic authorities to print increasingly large quantities to maintain government function. This external pressure creates acceleration that domestic policy cannot control.

Historical examples demonstrate that wars, fiscal crises, or political instability often provide the catalyst, but underlying monetary excess creates the vulnerability. Once foreign exchange markets lose confidence, the government faces impossible choices between hyperinflation and complete economic shutdown.

How Quickly Can Currency Debasement Accelerate?

Historical analysis reveals acceleration from gradual to hyperinflationary within 6-18 months once critical confidence thresholds are breached. The Weimar Republic experienced 22 months from initial acceleration to peak crisis, while Zimbabwe’s collapse occurred over 8 years with final acceleration in the last 18 months.

Velocity increases provide the primary acceleration mechanism. When people expect currency depreciation, they spend money immediately rather than holding it, increasing circulation speed and amplifying price effects. Modern electronic payment systems potentially accelerate this process beyond historical precedents.

What Percentage of Wealth Should Be in Hard Assets?

Allocation depends on individual circumstances, but historical analysis suggests 15-25% in precious metals during periods of monetary instability provides optimal risk-adjusted returns. Conservative investors may prefer 5-10% during normal conditions, while those anticipating crisis scenarios might allocate 30-40%.

The key principle involves treating precious metals as insurance rather than speculation. Like any insurance, the cost appears unnecessary until protection becomes critical. Gradual accumulation during stable periods provides better average prices than crisis-driven purchases.

Consequently, understanding gold safe haven insights becomes crucial for implementing effective allocation strategies during uncertain monetary environments.

Can Governments Confiscate Private Gold Holdings?

Executive Order 6102 in 1933 demonstrates historical precedent for gold confiscation in advanced democracies. However, enforcement proved difficult even with smaller populations and less global mobility. Modern storage options enable geographic diversification that reduces single-jurisdiction risk.

Contemporary confiscation would likely target electronic records and institutional holdings rather than private physical possession. Maintaining some allocation in foreign storage jurisdictions provides protection against domestic policy changes while preserving accessibility.

How Do Precious Metals Perform During Deflationary Periods?

While nominal prices may decline during deflation, precious metals often increase in purchasing power as goods and services fall faster than metal prices. The critical distinction involves deflation caused by productivity gains versus debt liquidation.

Productivity-driven deflation typically benefits all holders of money-like assets, including precious metals. Debt liquidation deflation, however, often leads to currency system stress, benefiting hard assets despite short-term price volatility. The 1930s demonstrated this pattern, with gold maintaining value while most assets collapsed.

Further Exploration:

Understanding monetary systems and precious metals requires ongoing education beyond any single article. Readers seeking deeper knowledge can explore additional resources such as educational content on monetary history, which offers comprehensive perspectives on currency systems and wealth preservation strategies across different historical periods and economic environments.

Ready to Position Yourself Ahead of Monetary System Changes?

Discovery Alert’s proprietary Discovery IQ model provides instant notifications on significant ASX mineral discoveries, helping investors identify actionable opportunities in precious metals and mining companies before broader market recognition. With major currency debasement trends accelerating globally, subscribers gain crucial insights into ASX mineral discoveries that historically deliver substantial returns during monetary instability. Begin your 14-day free trial today to secure your market-leading advantage in these uncertain economic times.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment