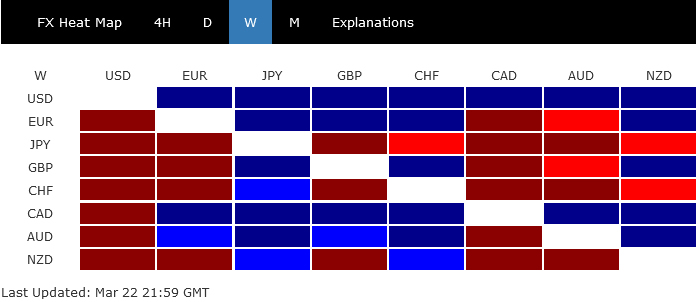

Dollar Triumphs Following a Turbulent Week of Central Bank Shocks

The past week in the currency markets was a dramatic whirlwind, marked by pivotal moves from major central banks across the globe. From BoJ’s unexpected hike to SNB’s surprise cut, from Fed’s hawkish leaning projections to BoE’s dovish voting, they collectively orchestrated a much volatile than usual trading environment.

Amidst this chaos, Dollar emerged victorious as the best performer. The technical picture in Dollar index suggests that more upside is likely in the greenback for the near term. Conversely, Swiss Franc and Japanese Yen bore the brunt of these developments, ending the week as the two worst performers by a mile. However, their late recovery indicate short-term stabilization, offering a reprieve from their downward spirals.

As the dust settles, attention shifts towards identifying the next currency at risk of an intensified downturn. British Pound is a candidate following BoE’s dovish pivot, which has ignited speculation about rate cut as soon as June. At least, it’s probably now already in a near term bearish reversal against Euro.

Furthermore, while New Zealand Dollar has already been under pressure due to concerns over the nation’s economic outlook, as voiced by New Zealand’s Finance Minister, Australian Dollar might be next in line. The steep plunge in Chinese Yuan last week, if sustained, could precipitate a broader sell-off in the stock markets of China and Hong Kong, adversely affecting Aussie in the process.

Dollar Dominates After Fed’s Hawkish Tilt

Following a turbulent week, Dollar eventually asserted its dominance and ended as the stronger performer. The new dot plot accompanying Fed’s rate decision to keep rate steady at 5.25-5.50% might have initially perceived as dovish. Fed maintained the projection of three rate cuts this year, tentatively placing the first reduction in June.

Upon a more detailed review, however, it became apparent that Fed’s stance had subtly shifted towards a more hawkish orientation instead. This shift is illustrated by a nearly even split among FOMC members, with nine anticipating two rate cuts and ten forecasting three within the year—a notable change from December’s 8-11 split. Furthermore, Fed’s projections suggest a more gradual path to easing, with the federal funds rate expected to decrease to 3.875% by the end of 2025 (vs prior 3.625%) and 3.125% by the end of 2026 (vs prior 2.875%). This revised outlook, including a slight increase in the long-term federal funds rate estimate from 2.5% to 2.6%, indicates that the projections are clearly not dovish at all.

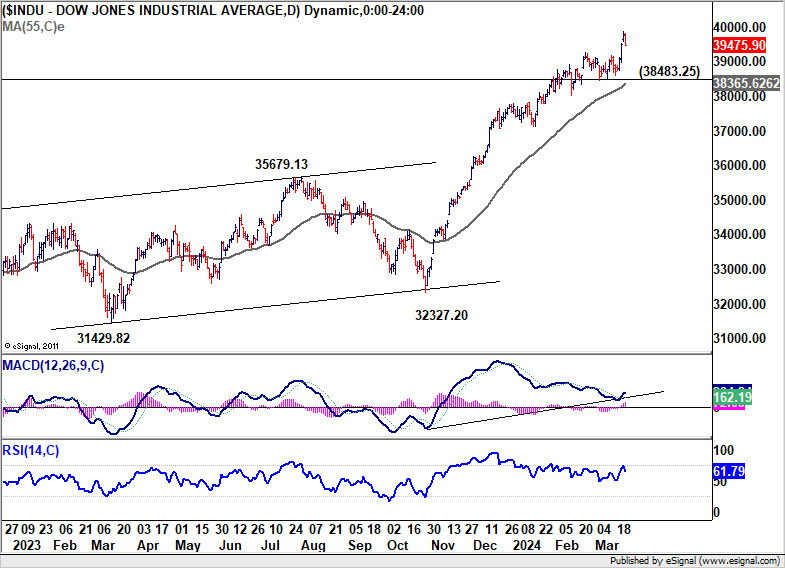

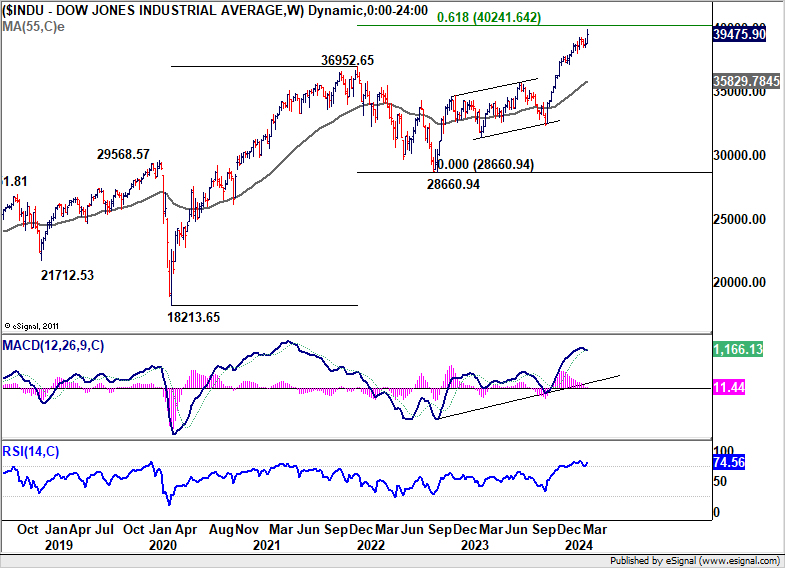

Regarding market reactions, DOW surged to new record high at 39889.05 last week. While DOW ended -305 pts lower on Friday, it still notched the best week since December. Next term outlook will stay bullish as long as 38483.25 support holds. The question is whether DOW has enough momentum to rise through 40k handle sustainably, considering that 61.8% projection of 18213.65 to 36952.65 from 28550.94 at 40251.64 is around.

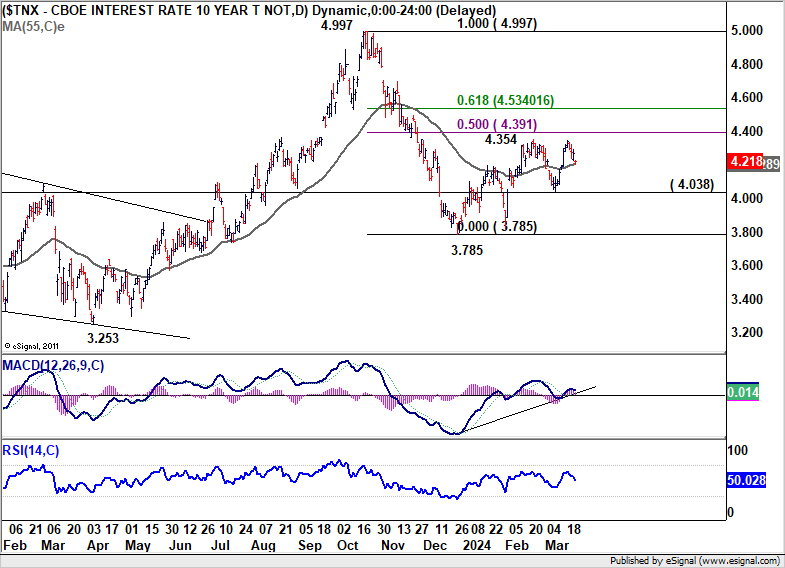

10-year yield failed to break through 4.354 resistance and restreated to close at 4.218. For now, it looks like the range is set for some sideway trading for the near term, between 4.038 and 50% retracement of 4.997 to 3.785 at 4.391. Or in short, the range is set between 4.0-4.4. Break of 4.000 is unlikely until there is firm indication that Fed’ easing has started.

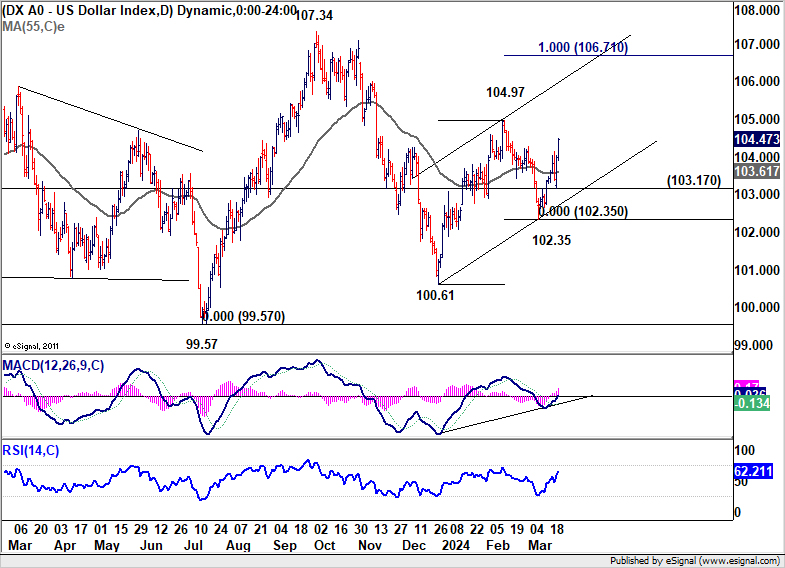

Dollar Index’s strong rally suggests that pull back from 104.97 has completed at 102.35 already. Rise from there is likely resuming the rise from 100.61, which is the third leg of the pattern from 99.67 low. Near term outlook will stay cautiously bullish as long as 103.17 support holds. Break of 104.97 should pave the way to 100% projection of 100.61 to 104.97 from 102.35 at 106.71.

BoJ’s Rate Increase Marks a Historic Shift, Yet Steady Tightening Is Not Imminent

Investors responded very positively to BoJ’s surprised move to raise its interest rate to 0-0.1% and conclude its long-standing Yield Curve Control policy. This historic adjustment sent shockwaves through the markets, propelling Nikkei to unprecedented heights while concurrently sending Yen into a nosedive.

The reactions reflected market’s interpretation of BoJ’s actions as a strategic overhaul of the monetary policy framework, rather than the commencement of a sustained tightening cycle. While there are talks around the possibility of another rate hike in the latter half of the year, such discussions remain speculative at this juncture.

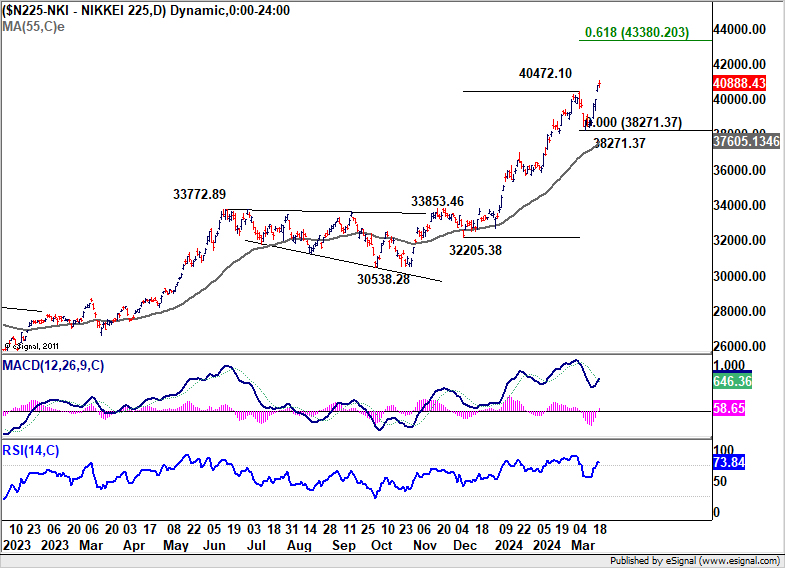

Nikkei’s up trend resumed last week and hit as high as 41087.75. Near term outlook will stay bullish as long as 38271.37 support holds. Next target is 61.8% projection of 32205.38 to 40472.10 from 38271.37 at 43380.23. There is prospect of topping around this projection level to end the five wave rally from 30538.28, to start a medium term correction phase.

BoE’s Dovish Pivot, FTSE Gains Momentum

While BoE left interest rate unchanged at 5.25% last week, the voting and subsequent comment from Governor Andrew Bailey were seen as a dovish pivot, setting the stage for the start of interest rate reduction later in the year. Firstly hawks Jonathan Haskel and Catherine Mann dropped their votes for hike this round, while Swati Dhingra advocating for a reduction again, making it an 8-1 split to stand pat.

Bailey’s remarks reinforced this perspective, acknowledging the market’s expectations for three rate reductions within the year as “reasonable.” This commentary has led to increased speculation in financial markets, June is now seen as a possibility for the first cut, with bets now fully pricing in by August. Further, markets are anticipating a total of three reductions by the year’s end, which would lower rates to 4.5% by December.

FTSE, the laggard index comparing to DOW, DAX and CAC, appeared to be finally catching up. The strong rally last week suggests that triangle consolidation from 8047.06 has completed, larger up trend could be ready to resume. Near term outlook will now stay bullish as long as 7785.73 resistance turned support holds. 61.8% projection of 6707.62 to 8047.06 from 7404.08 at 8231.85 would be the key level to determine FTSE’s underlying medium term momentum.

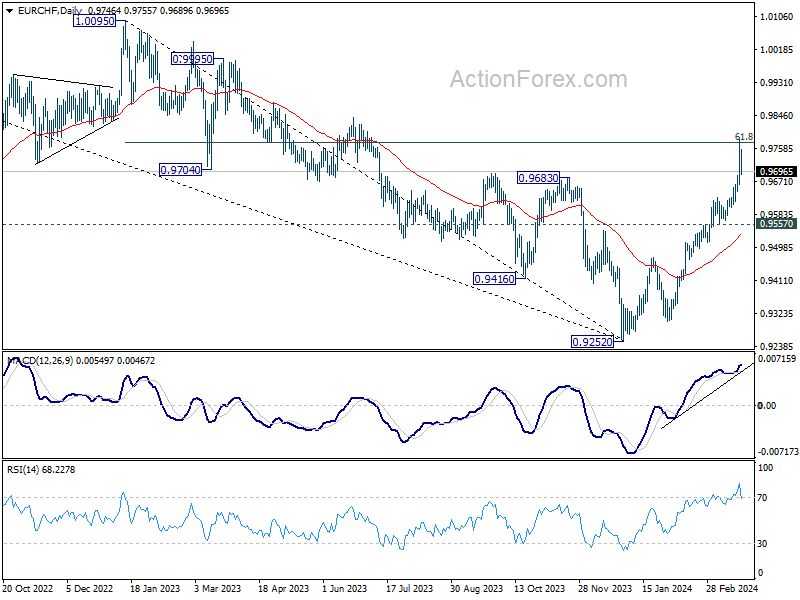

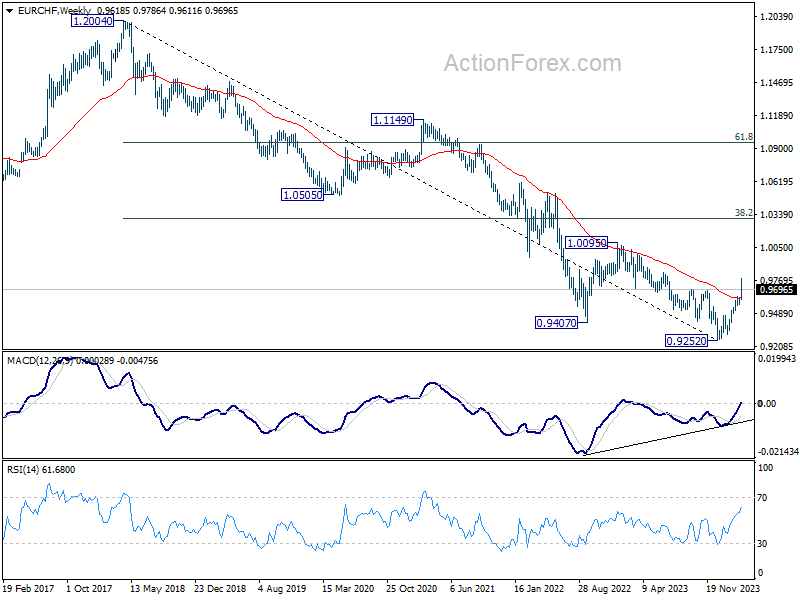

Swiss Franc’s Bearish Turn after SNB’s Rate Cut

Swiss Franc was sold off deeply after SNB’s surprised rate cut, and ended as the worst performer. Franc’s late recovery may hint that the initial selling frenzy might have peaked. However, that could only offer a momentary respite for the France as the bearish trend has likely been established already.

EUR/CHF rose to as high as 0.9786 but retreated after hitting 61.8% retracement of 1.0095 to 0.9252 at 0.9773. Some consolidations would be seen below this level in the near term. But downside of retreat should be contained above 0.9557 support to bring rebound.

The strong break of 55 W EMA argues that a medium term bottom was formed at 0.8252 on bullish convergence condition in W MACD. Rise from there should now target 1.0095 resistance or further to 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even as a corrective bounce in the long term down trend.

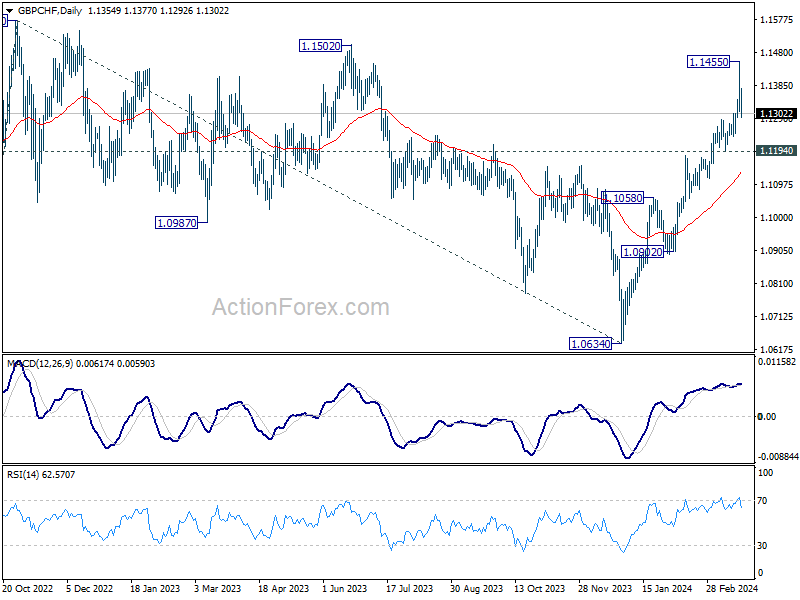

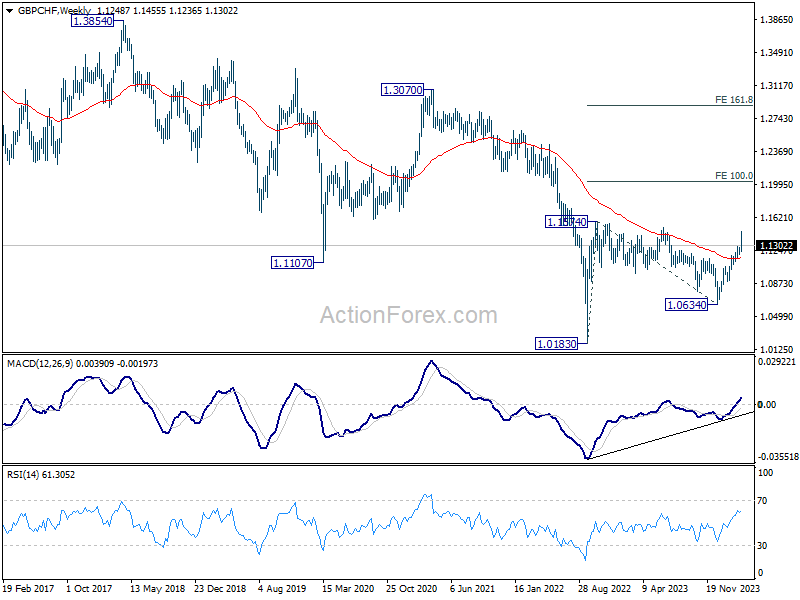

GBP/CHF also retreated after rising to 1.1455. Some consolidations is likely in the near term, but downside of retreat should be contained above 1.1194 support to bring rebound.

Current development affirms the case that rise from 1.0634 is resuming whole rally from 1.0183. Break of 1.1574 resistance will confirm and target 100% projection of 1.0183 to 1.1574 from 1.0634 at 1.2025 in the medium term.

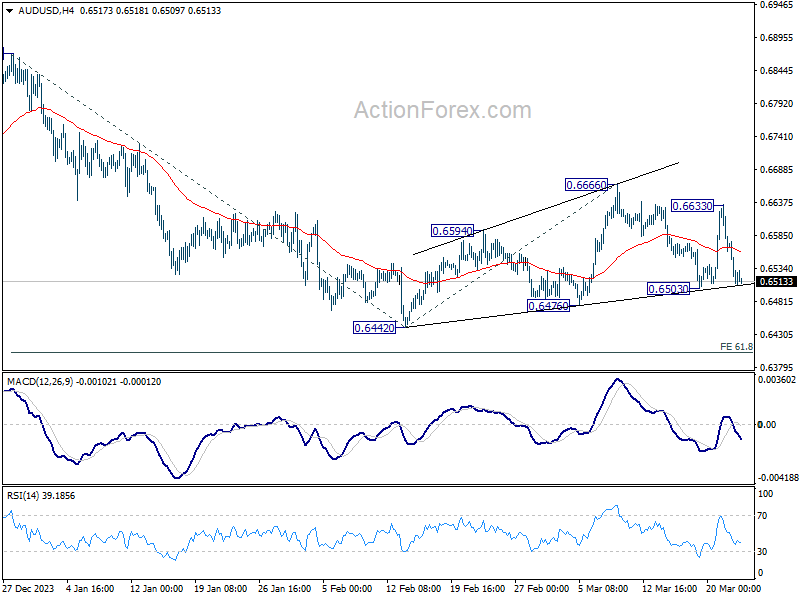

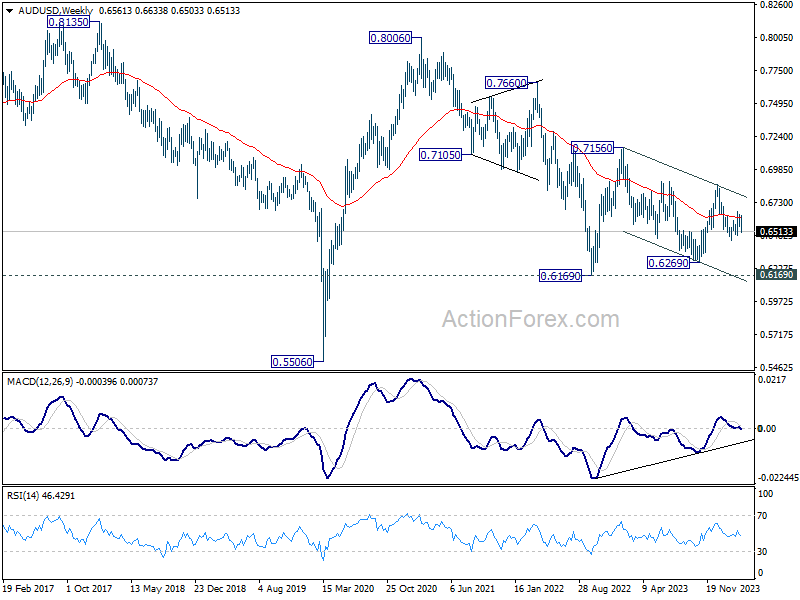

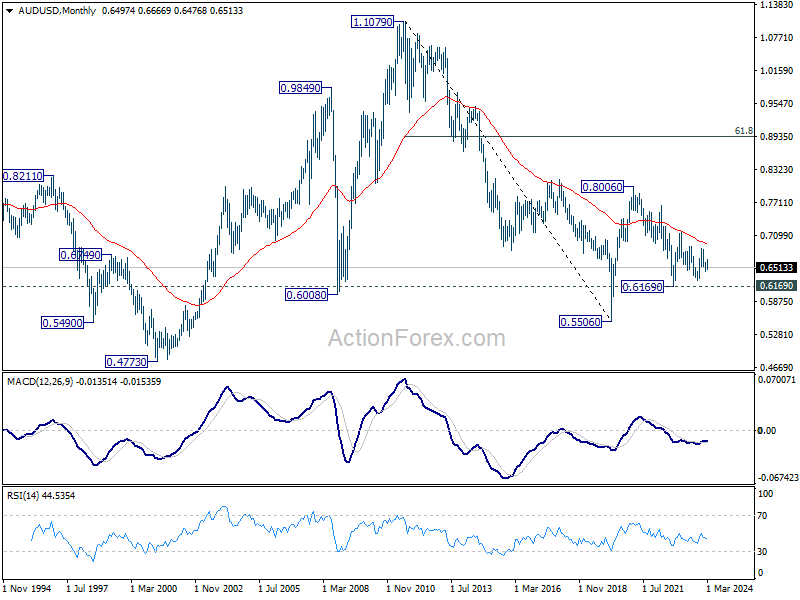

AUD/USD Weekly Report

AUD/USD’s strong was rebound last week was capped below 0.6666 resistance, and followed by equally steep decline. Initial bias remains neutral this week first, with focus on 0.6503 support. Decisive break there will indicate that larger fall from 0.6870 is ready to resume, and turn bias to the downside for 0.6442 low. For now, risk will stay on the downside as long as 0.6633 resistance holds, in case of recovery.

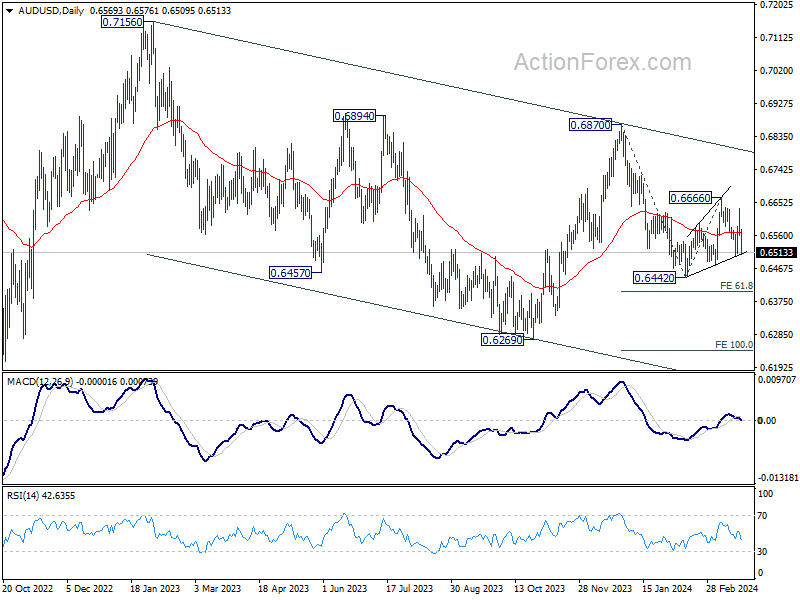

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which might still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

In the long term picture, the down trend from 1.1079 (2011 high) should have completed at 0.5506 (2020 low) already. It’s unsure yet whether price actions from 0.5506 are developing into a corrective pattern, or trend reversal. But in either case, fall from 0.8006 is seen the second leg of the pattern. Hence, in case of deeper decline, strong support should emerge above 0.5506 to bring reversal.

Source link