Fed Won’t Cut Rates in 2024 Warns Apollo

Above: File image of Torsten Sløk. Image copyright: Danish Maritime Days.

The Dollar may surge if the market realises that the Federal Reserve won’t cut interest rates in 2024, as now anticipated by a major American money manager.

Apollo Global Management says it now expects the Federal Reserve to hold interest rates unchanged for the remainder of 2024; if correct, the call carries deep implications for financial markets, given investors walked into 2024 expecting six Fed rate cuts.

The Dollar strengthened in January and February as markets realised the U.S. economy was too strong to warrant rate cuts as soon as March, and a subsequent rerating in expectations means just three cuts are now expected, the first falling in June.

“The reality is that the US economy is simply not slowing down, and the Fed pivot has provided a strong tailwind to growth since December,” says Torsten Sløk, Chief Economist at Apollo. “As a result, the Fed will not cut rates this year, and rates are going to stay higher for longer.”

Apollo is a New York-listed financial services firm with half a trillion dollars under management.

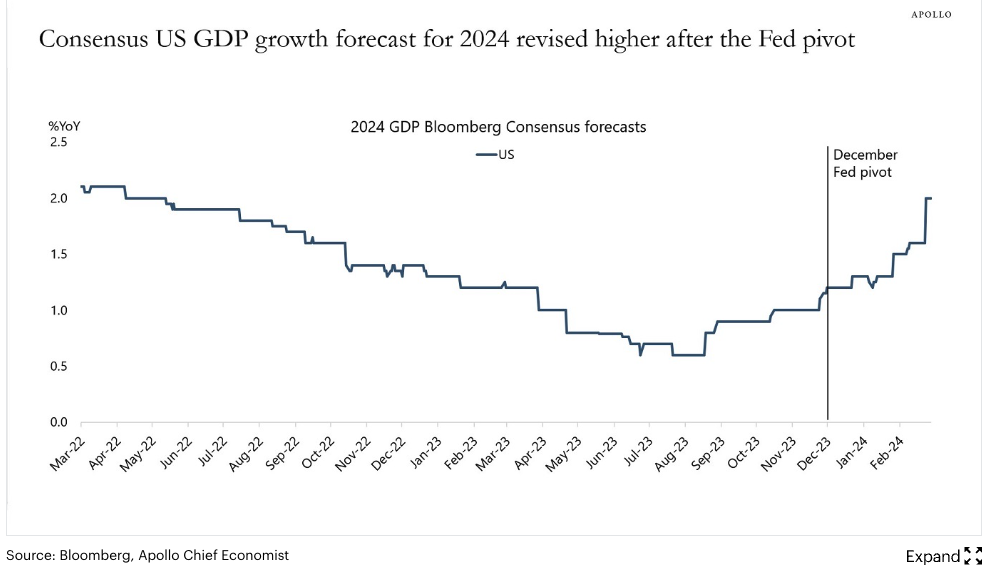

The market still sees the first Fed rate cut in June, but Sløk says the economy is reaccelerating. “Growth expectations for 2024 saw a big jump following the Fed pivot in December and the associated easing in financial conditions. Growth expectations for the U.S. continue to be revised higher,” he says.

The Fed pivot he references is the Fed’s December meeting, where it acknowledged for the first time that the next move on rates would be a cut. This saw money markets price in lower U.S. Fed rates, which brought down bond yields and the cost of money more broadly.

Therefore, expectations can have real-world impacts, and in this instance, the Fed’s communication stimulated the economy.

“Financial conditions continue to ease following the Fed pivot in December with record-high IG issuance, high HY issuance, IPO activity rising, M&A activity rising, and tight credit spreads and the stock market reaching new all-time highs. With financial conditions easing significantly, it is not surprising that we saw strong nonfarm payrolls and inflation in January, and we should expect the strength to continue,” says Sløk.

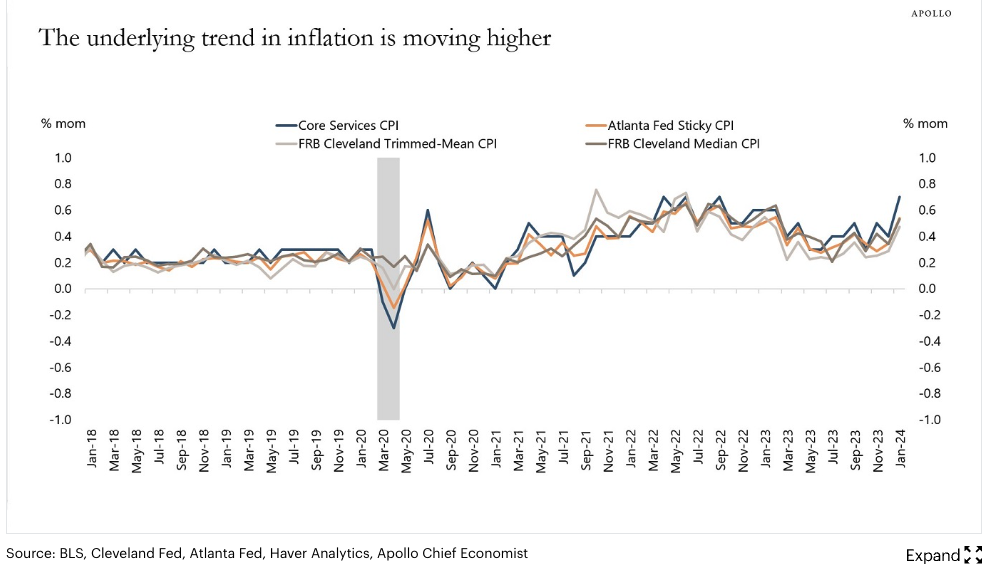

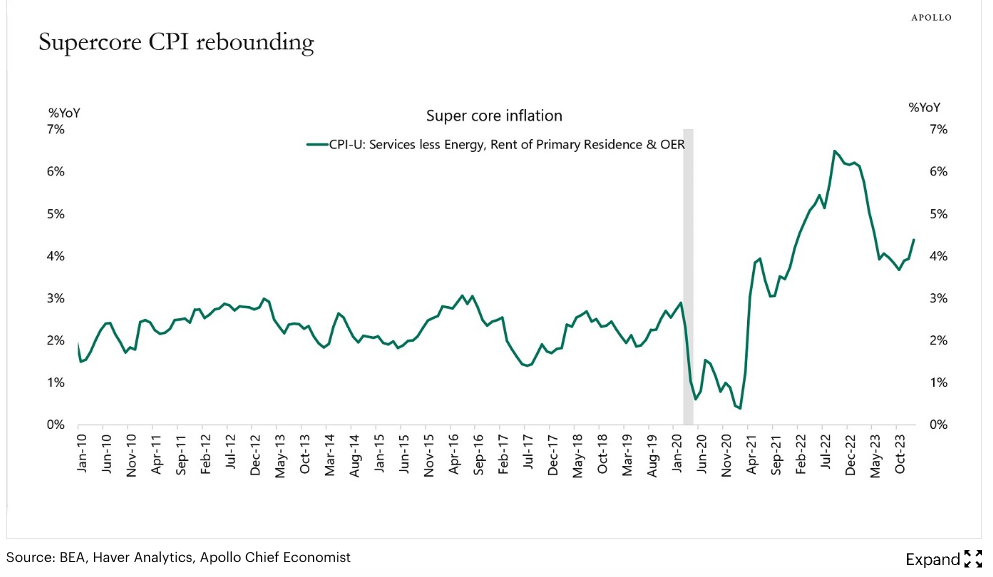

Sløk says underlying measures of trend inflation are moving higher in the U.S. and supercore inflation, a measure of inflation preferred by Fed Chair Powell, is trending higher.

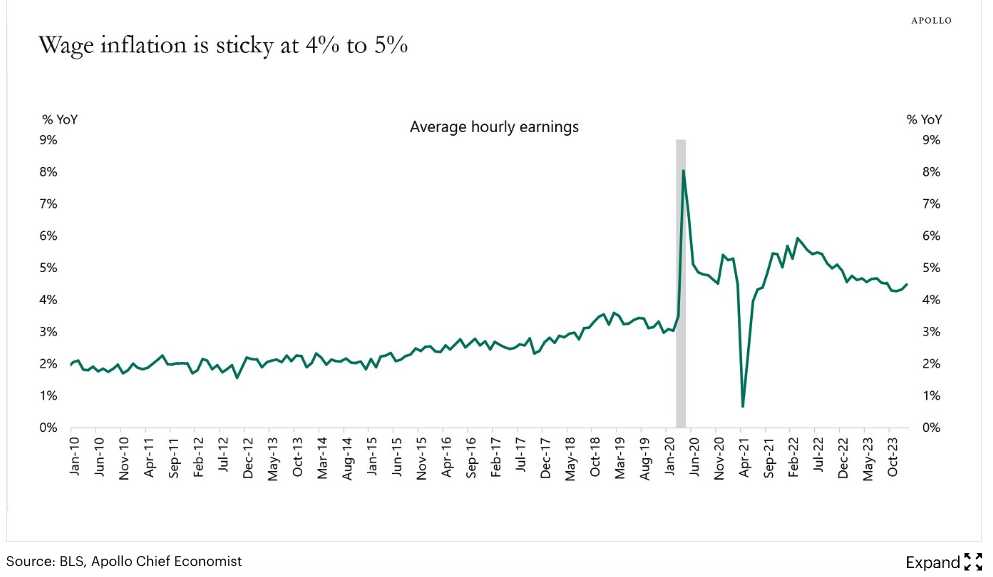

He also points out that the U.S. labour market remains tight, jobless claims are very low, and wage inflation is sticky between 4% and 5%. Economists agree that the labour market must ‘loosen’ before home-made inflation rates can cool.

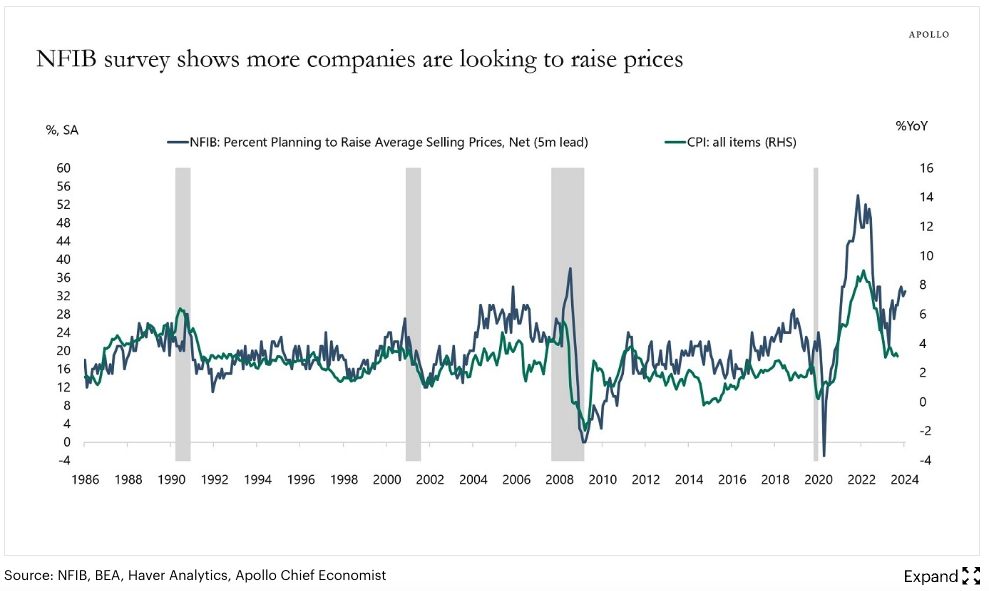

Meanwhile, surveys of U.S. small businesses show that more small businesses are planning to raise selling prices. This intention to raise prices is coming up in other surveys, which are cited by Sløk:

Manufacturing surveys show a higher trend in prices paid, another leading indicator of inflation, ISM services prices paid is also trending higher. Surveys of small businesses show that more small businesses are planning to raise worker compensation.

The housing sector is also showing worrying trends that would preclude a rate cut: “Asking rents are rising, and more cities are seeing rising rents, and home prices are rising,” says the analyst.

“The bottom line is that the Fed will spend most of 2024 fighting inflation. As a result, yield levels in fixed income will stay high,” says Sløk.

If Apollo is Right, What Will Happen to the Dollar?

The Dollar is 2024’s best-performing currency amidst the ‘pricing out’ of three rate cuts; however, the moves in FX have been relatively contained.

For instance, the Pound to Dollar exchange rate has traded in an unusually tight range, while the Euro to Dollar exchange rate has recovered from its lows and is stuck around 1.08. The limited volatility is the result of the market expecting the world’s major central banks to begin cutting together in mid-year.

For markets to remain becalmed, other central banks would have to delay their own cuts alongside the Fed. This is unlikely, and we suspect that a complete evaporation of Fed rate cut expectations would shake the market and introduce more volatility.

Financial conditions would tighten and potentially lead to a meaningful stock market selloff that would boost the Dollar as investors demand safe-haven currencies.

Moreover, global central banks like the Bank of England and the European Central Bank would almost certainly be unable to delay too long and would raise interest rates ahead of the Fed as it becomes clear domestic conditions warrant it.

With Eurozone growth already running below potential and creating an output gap, the ECB will surely have to cut before the Fed.

Above: Low-volatility in the FX market won’t last for much longer: Société Générale.

The Bank of England could afford to be more patient, given markets are already well acquainted with the notion that the UK has sticky inflation rates. Data also suggests the UK economy has picked up pace in early 2024, mirroring the U.S. (Some researchers point out that the UK is tracking the U.S. cycle owing to a significant upsurge in service exports to the U.S. from the UK in recent years).

This suggests that Euro-Dollar would have greater downside potential than Pound-Dollar (resulting in a higher Pound-Euro) if the Fed opts not to cut in 2024.

Whether Apollo is correct will become known sooner rather than later: March’s U.S. labour market report (next Friday) and inflation report (mid-month) will be critical.

Another round of hot readings will hammer home to the market that thinkers like Apollo are right. If so, expect the FX market to wake up from its current low-volatility slumber.

Source link