‘Magnificent Seven’ Power AI-Driven Stock Rebound: Markets Wrap

(Bloomberg) — Tech giants led gains in stocks at the start of a week that will bring a raft of central-bank decisions from the US to England and Japan.

Most Read from Bloomberg

The megacap space outpaced the broader market. Alphabet Inc. jumped as Bloomberg News reported Apple Inc. is in talks to build Google’s Gemini artificial-intelligence engine into the iPhone. Just ahead of Nvidia Corp.’s AI conference — and chief Jensen Huang’s keynote — expectations are high for the chipmaker to deliver news that will sustain its blistering rally.

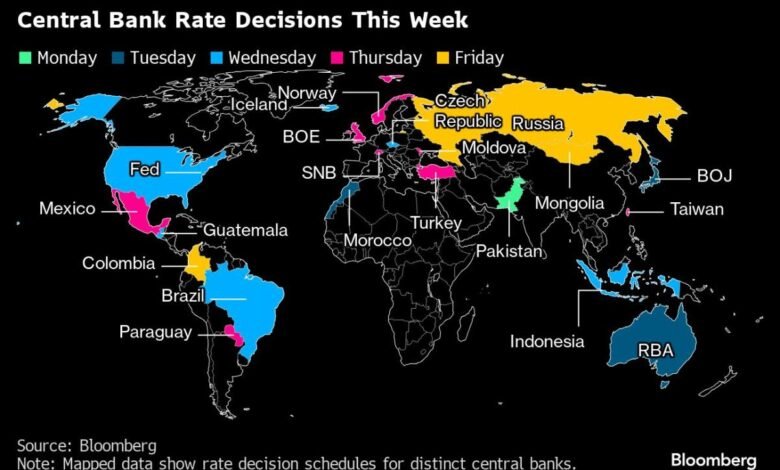

Investors may glean more on the Federal Reserve’s resolve to ease and how close Japan is to finally exiting negative interest rates as central banks set policy for almost half the global economy. The coming week features the world’s biggest agglomeration of decisions for 2024 to date, including judgments on the cost of borrowing for six of the 10 most-traded currencies.

“It’s a jam-packed week of central bank meetings,” said Win Thin and Elias Haddad at Brown Brothers Harriman. “There are sure to be some surprises and so today’s calm is likely to give way to greater volatility ahead.”

The S&P 500 halted a three-day slide, the Nasdaq 100 rose 1.5% and a gauge of the “Magnificent Seven” tech megacaps climbed over 2%. US two-year yields hit 2024 highs as expectations for Fed cuts continued to erode. The yen fluctuated after a news report the Bank of Japan is poised to decide to end its policy of guiding government bond yields — known as yield curve control.

Ahead of the Fed decision, Japan will face a monumental moment in its history — with the nation expected to end its negative interest rate regime — the world’s last. Traders betting on the outcome of the BoJ’s decision have boosted their positions in yen futures to the highest since 2007.

Bank of America Corp. strategists said that an end to YCC would only have a limited impact on the appetite for US Treasuries.

Bond investors who were once convinced that the Fed would start cutting rates this week are painfully surrendering to a higher-for-longer reality. Treasury yields have climbed as data continued to point to persistent inflation, causing traders to push back their timetable for US monetary easing. Swaps are currently pricing in less than 50% odds of a June rate cut.

Goldman Sachs Group Inc. economists led by Jan Hatzius changed their forecast to call for three quarter-point Fed cuts this year — instead of four. The change, which brings the forecast in line with the median forecast policymakers made in December, is “mainly because of the slightly higher inflation path,” they said.

“After last week’s double-dose of hot inflation data, everyone will be wondering whether the Fed is rethinking a June cut,” said Chris Larkin at E*Trade from Morgan Stanley. “The market will need to like what it sees in the Fed’s statement on Wednesday, and get confirmation from Jerome Powell that two months of sticky inflation numbers won’t derail the Fed’s game plan.”

Investors will be keenly focused on the US central bank’s projections — the dot plot — to gauge how many rate cuts policymakers are expecting to deliver this year.

To Krishna Guha at Evercore, the Fed will firm up its tone following hotter inflation reports – but will continue to point to a market-friendly base case of three cuts this year starting June.

“We think he will say the Committee will be patient and take as long as needed to accumulate sufficient confidence – underlining June is not guaranteed and the Fed would delay to July/September if necessary, Guha noted.

Traders will also be interested to see whether the Fed changes its views for 2025-2026 and the “neutral rate” — the level seen as neither stoking growth or holding it back.

“The Fed has been quite reluctant to change their neutral rate estimate,” said Neil Dutta at Renaissance Macro Research. “Raising neutral would be one way to signal to markets that a deep easing cycle is unlikely.”

Wall Street will listen carefully to any signs from Powell on the phase out of quantitative tightening, known as QT. While a handful expect the Fed to announce or even begin slowing the unwind of its balance sheet as early as May, others don’t see a tapering starting until the second half of the year.

It looks like the Fed will begin to taper QT this year — and hints to that effect could be a positive for Treasury markets — allowing yields to drift sideways or down, according to David Kelly at J.P. Morgan Asset Management.

“For investors, this isn’t exactly a rallying cry to buy bonds,” Kelly noted. “However, it does suggest the potential for a relatively stable financial environment, allowing equities to continue to move higher and fixed income to play its traditional role of providing income and diversification to portfolios.”

US stocks will beat Treasuries over the next month, according to the latest MLIV Pulse survey. That’s the fifth consecutive poll in which majority of respondents opted for equities, the longest streak of pro-stocks bias since the survey started asking the question in August of 2022.

Recent data has painted an ambiguous picture about the growth and inflation trends in the US economy, but it’s best not to over-analyze each data point and instead be clear-headed about the general direction of travel, said Jason Draho at UBS Global Wealth Management.

“It’s a fairly healthy US macro environment, and it should stay that way,” Draho said. “The Fed is likely to communicate the same message this week, and it seems inclined to do what it can to support that outlook. This is directionally positive for financial markets, and that’s not even accounting for the AI tailwind. Speed bumps, or turbulence, more aptly, aren’t enough to derail the soft-landing trajectory.”

In earnings this week, FedEx Corp.’s outlook on Thursday will provide hints on the state of the US economy after the bellwether previously forecast a slight revenue decline this fiscal year because of “volatile macroeconomic conditions.”

Nike Inc., Lululemon Athletica Inc., General Mills Inc., and Darden Restaurants Inc. results will show whether consumers are pulling back on spending or trading down, especially with inflation hanging around.

Corporate Highlights:

-

Nasdaq Inc. said it has resolved a technology glitch that disrupted premarket trading for almost three hours.

-

The boss of Exxon Mobil Corp. said Monday that it has no interest in buying Hess Corp. outright, despite taking Chevron Corp. to arbitration over its proposed $52 billion merger with the other company.

-

Fisker Inc. is pausing production for the next six weeks as the electric-vehicle maker looks to rein in inventory and avoid possibly having to file for bankruptcy.

-

B. Riley Financial Inc., the boutique investment bank under attack from short sellers about its dealings with a former business partner, failed to file its audited results after an extension period ended.

-

PNC Financial Services Group Inc. announced Monday that it’s launched a national advertising campaign to persuade customers that its bank is “brilliantly boring.”

-

The head of United Airlines Holdings Inc. told customers that the carrier is reviewing a series of recent mishaps involving its planes, promising any lessons learned would “inform our safety training and procedures” across the company.

-

Barclays Plc is seeking to expand its relationships with sovereign wealth funds and private equity giants as part of its efforts to improve the profitability of its investment banking division by expanding in advisory and equity underwriting.

-

Encyclopaedia Britannica Inc., the education technology company and publisher of books including the Merriam-Webster dictionary, is seeking a valuation of about $1 billion its initial public offering, according to people with knowledge of the matter.

Key events this week:

-

Bank of Japan rate decision, Tuesday

-

Germany ZEW survey expectations, Tuesday

-

European Central Bank Vice President Luis de Guindos speaks, Tuesday

-

US housing starts, Tuesday

-

Eurozone consumer confidence, Wednesday

-

Fed rate decision; Chair Jerome Powell holds news conference, Wednesday

-

Reddit’s IPO, Wednesday

-

ECB’s Christine Lagarde speaks, Wednesday

-

Eurozone S&P Global Services PMI, S&P Global Manufacturing PMI, Thursday

-

Bank of England rate decision, Thursday

-

US Conference Board leading index, existing home sales, initial jobless claims, Thursday

-

Nike, FedEx earnings, Thursday

-

Japan CPI, Friday

-

Germany IFO business climate, Friday

-

Atlanta Fed President Raphael Bostic speaks, Friday

-

ECB’s Robert Holzmann and Philip Lane speak, Friday

Some of the main moves in markets:

Stocks

-

The S&P 500 rose 0.9% as of 2:31 p.m. New York time

-

The Nasdaq 100 rose 1.4%

-

The Dow Jones Industrial Average rose 0.4%

-

The MSCI World index rose 0.7%

Currencies

-

The Bloomberg Dollar Spot Index rose 0.2%

-

The euro fell 0.2% to $1.0870

-

The British pound was little changed at $1.2726

-

The Japanese yen was unchanged at 149.04 per dollar

Cryptocurrencies

-

Bitcoin fell 1.6% to $67,177.54

-

Ether fell 3.8% to $3,496.08

Bonds

-

The yield on 10-year Treasuries advanced three basis points to 4.34%

-

Germany’s 10-year yield advanced two basis points to 2.46%

-

Britain’s 10-year yield declined one basis point to 4.09%

Commodities

-

West Texas Intermediate crude rose 2% to $82.69 a barrel

-

Spot gold rose 0.2% to $2,159.58 an ounce

This story was produced with the assistance of Bloomberg Automation.

–With assistance from Kasia Klimasinska, Robert Fullem, Carter Johnson, Ye Xie, Michael Mackenzie, Alexandra Harris, Jan-Patrick Barnert, Michael Msika, Craig Stirling and Felice Maranz.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.

Source link