Should you use a HELOC to pay off your mortgage?

Key takeaways

-

Using a HELOC to pay off your mortgage can be a strategic move, especially if you have a lot of equity in your home and a small outstanding balance.

-

Opening a HELOC to pay off your home loan will still leave you with an outstanding debt and interest — and unlike most mortgages, HELOCs have variable interest rates, which can increase.

-

Alternatives to the HELOC strategy to pay off a mortgage include home equity loans or just making bigger or extra payments on your existing mortgage.

Many homeowners today are sitting on significant equity in their homes: As of Q1 2024, the average mortgage holder now has $299,000 in equity, according to ICE Mortgage Technology, which tracks real estate data. If you’re one of them, you might be wondering if it makes sense to use a home equity line of credit (HELOC) to pay off your mortgage — especially if the remaining balance is fairly small.

Here’s what to know about paying off your mortgage with a HELOC — and the risks that come with this strategy.

Is it a good idea to pay off your mortgage early with a HELOC?

Prepaying your mortgage can certainly save you money in the long run. However, using a home equity line of credit (HELOC) to do so has limitations.

First of all, lenders typically only allow you to borrow up to 80 percent (sometimes 85 percent) of your equity in your home via a line of credit. Depending on your specific financials, this might not be enough to pay off your mortgage entirely.

Secondly, whatever funds you use from the HELOC need to be paid back: The repayment period typically lasts 20 years. If you’re close to paying off your current mortgage, you might not want to commit to repaying another debt over two more decades, especially if you’re nearing or in retirement and on a fixed income. (Of course, there’s no law that says you can’t settle the HELOC balance early, though there may be a prepayment fee to do so.)

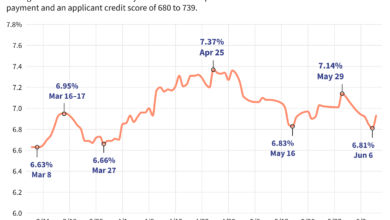

But the biggest reason to pause: interest rates. Although they both use your home as collateral, HELOCs tend to be the more expensive form of financing. Currently, their interest rates are hovering around 9 percent, compared to 7 percent for the average 30-year mortgage, purchase or refinance. Also bear in mind that, unlike most mortgages, most HELOCs have fluctuating interest rates — and rates have been on the rise since 2022, reflecting the Federal Reserve’s series of rate hikes to contain inflation. While HELOC rates are projected to fall in 2024, a lot can change over two decades.

That means interest rates on an older mortgage may remain competitive against a HELOC taken out today. “Variable-rate HELOC customers could easily see their interest rates rise significantly,” says Herman (Tommy) Thompson, Jr., CFP, of Innovative Financial Group in Atlanta. “It’s also unlikely that the interest rate on a [new] HELOC would actually be lower than a mortgage acquired in the past 20 years.”

How to use a HELOC to pay off your mortgage

1. Shop for a competitive rate

If you’re considering the HELOC strategy to pay off a mortgage, it all comes down to rates. Evaluate different options and investigate what HELOC rate you qualify for. Compare the rates and terms available against your current mortgage to determine whether you would benefit from taking this step. Remember, HELOCs come with variable rates, so you want a big margin with room for upward direction.

2. Apply for a HELOC

If you find a HELOC with a favorable interest rate and terms, go ahead and apply. Typically, you will need at least 15 to 20 percent equity in your home, a credit score in the mid-600s, and a debt-to-income ratio of 43 percent or less to qualify for a HELOC.

3. Receive your HELOC funds

Expect a processing time of between two and six weeks from when you apply to when you receive access to your line of credit. Once you can access your line of credit, you can borrow against the available equity in your home either over your HELOC’s draw period or all at once.

4. Pay off your mortgage and maintain regular HELOC payments

Assuming you qualify for enough of a HELOC to pay your mortgage balance off in full, you can do so as soon as you have access to your home’s equity. Keep an eye out for documents confirming the closure of your mortgage loan, and focus on staying current with HELOC payments moving forward.

When to pay your mortgage with a HELOC

There’s no set equity amount or percentage of your remaining loan to pay down that indicates when you should use a HELOC to pay off a mortgage. Much depends on the amount of equity you started with — that is, how much of the home you paid for in cash/how big a down payment you made — and how much of your mortgage balance is outstanding. Obviously, the longer you’ve been making your payments, the more equity you’ve built up, and are able to tap.

Mainly, though, it all comes down to interest rates. You should only pay off a mortgage with a HELOC if you can get a significantly better interest rate on the line of credit than you currently have with your mortgage. Because the HELOC’s rate is variable, it needs to be much lower than your mortgage rate — with room to move upward before you hit that rate — for this move to make financial sense. And because HELOCs generally have higher rates than mortgages, you might be hard pressed to make this math work.

The Shred Method

One early American advocate of using HELOCs to pay off mortgages was fintech platform developer Adam Carroll, founder of The Shred Method. Essentially it’s a mortgage acceleration strategy that uses a home equity line of credit as a checking account. It involves opening a HELOC, pulling funds from it in lump sums to pay down your mortgage and allocating all of your discretionary income to, in turn, pay down the line of credit.

The idea is to leverage the lower interest rates typically offered by HELOCs compared to other types of debt — a sort of interest rate arbitrage. The approach helps lower your borrowing costs significantly, reducing the overall amount you pay in interest and eliminating mortgage debt sooner. The average “shredder” takes just over 4 years to pay off their mortgage, The Shred Method’s website claims.

The Shred Method uses software whose algorithm recommends when to apply the HELOC funds to your mortgage (or any other compound-interest debt for that matter) and how much the payment should be. It can be implemented at any point, though it’s most efficient to use it early in your mortgage term, when your payments go more towards interest than principal, Carroll has said in interviews. Of course, you could practice a version of it on your own, sans the software, though it takes a lot of discipline and commitment to the debt repayment plan.

When not to use a HELOC to pay off your mortgage

You should pass on using a HELOC to pay off your mortgage if the numbers don’t make sense: that is, if the interest rates on the home equity line of credit are higher than those on your current mortgage. Even if they’re lower now, the variable rate that comes with HELOCs means you could easily find yourself spending more in interest over time than with your current mortgage.

There’s also a tax consideration, if you itemize deductions on your return: Mortgage loan interest is deductible, but HELOC loan interest to repay a mortgage probably would not be (you need to use the funds to buy, repair or substantially improve your home).

Even if HELOC interest rates are substantially lower, consider where you are in your mortgage term. If it’s far enough along so that your payments are going mostly towards principal, you might want to stick with the loan. Why trade those in for paying HELOC interest?

Pros and cons of using a HELOC to pay off a mortgage

Benefits of using a HELOC to pay off your mortgage

-

Flexibility: HELOCs are a more flexible form of financing in that you can borrow only what you need versus the entire amount you were approved for. For instance, if you don’t want to use all of the HELOC funds to pay down your mortgage, you might decide to devote some of the money to home renovations or other expenses. You can also withdraw different amounts at different times.

-

Low or no closing costs: Although HELOC closing costs can range from 2 percent to 5 percent of the amount you’re borrowing (similar to a mortgage), some lenders offer no-closing-cost HELOCs. The cost of borrowing this money might be lower than other options you might be considering, like a cash-out refinance.

-

Chance for a lower rate: If your current mortgage has a higher interest rate and the HELOC has a lower rate, you can use the funds from the HELOC to pay off your mortgage sooner for less. This depends largely on the broader mortgage market, however — right now, rates are rising on all types of loans, including HELOCs.

Risks and downsides of using a HELOC to pay off a mortgage

-

Fluctuating interest: HELOCs come with a variable interest rate, which means your rate will fluctuate over time based on market conditions. There’s no way to predict whether your rate will move up or down in the future, so you’ll need to be prepared to fit higher payments into your budget.

-

More debt: While you can pay off a mortgage with a HELOC, you’d also be replacing that debt with another form of debt, and you might end up paying more interest than you would have with your current mortgage. This has implications for your credit score and finances — especially if it’s not helping you save money in the long run.

-

Fees and penalties: Many HELOCs have an annual fee, and some come with a prepayment penalty if you pay off what you borrow sooner than the repayment schedule dictates.

-

Tax disadvantage: If you itemize, your mortgage interest is tax-deductible. Your HELOC’s interest may not be if you’re using it for this purpose — generally, you’d need to be using the funds to “buy, build, or substantially improve the home.” Definitely check with a tax pro.

Alternatives to HELOCs to prepay or pay off a mortgage

If your goal is to repay your mortgage early, you’ll likely be better off making extra payments, if possible — especially in the current elevated-interest-rate environment. You might opt to pay extra in a lump sum, or begin making biweekly payments. Even one more payment a year can speed up the payoff process.

Or, if you need to borrow the funds, consider taking out a home equity loan to pay off your mortgage. With a home equity loan, you’ll get a fixed rate (versus a variable rate with a HELOC), which means your monthly payments won’t change. However, you’re still borrowing money to pay off borrowed money, which isn’t ideal, especially with interest rates as high as they are right now. You’ll also incur closing costs, as a home equity loan is a second mortgage.

The bottom line on using a HELOC to pay your mortgage

A home equity line of credit is a powerful resource in your toolkit for achieving financial goals like consolidating debt, which could include paying off your mortgage. With this strategy, essentially you’re using your ownership stake in your home to pay off what you still owe on your home. But you’ll then have your HELOC debt to repay.

So, this approach only makes sense if you can get a significantly lower rate on a HELOC than you currently have on your home loan. But at their current interest rates, HELOCs are no longer super-cheap: The costs will likely outweigh the benefits, which means you’re better off waiting before deploying the HELOC strategy.

Learn more: How much equity can you get out of your home?

Additional reporting by Kacie Goff

Source link