Hong Kong property: homebuyers flock to Wheelock’s Seasons Place in Tseung Kwan O

“A new batch of units are expected to be launched in the short term, and there will be room for price increases,” Wheelock executive director Ricky Wong said in reaction to the strong market sentiment.

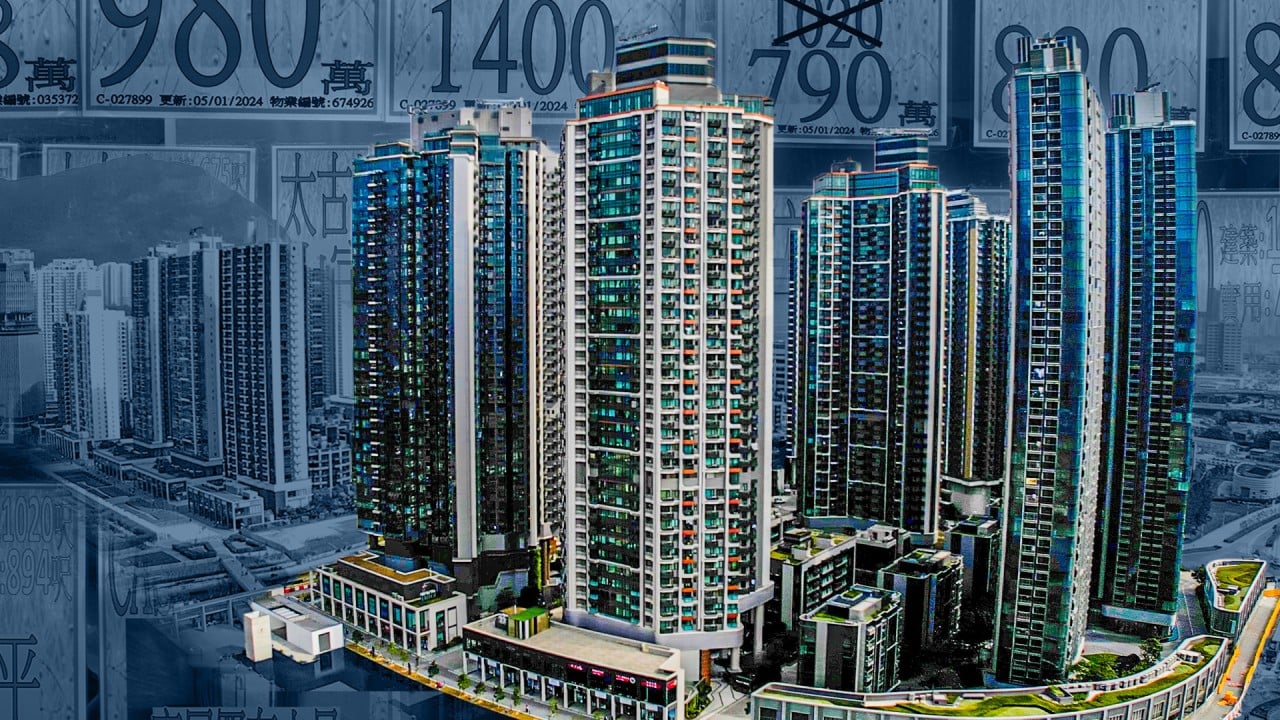

Even before the sale on Saturday, the project had attracted more than 10,000 prospective buyers who put down deposits. About 20 per cent of the buyers are from mainland China, according to the developer.

Wheelock priced the flats at a five-year low for the district, aligning with peers who continue to offer discounts to woo buyers in the wake of the government’s policy stimulus.

The units at Seasons Place include up to three bedrooms, with areas ranging from 323 to 665 sq ft. The price after discounts has been set between HK$4.47 million and HK$10.8 million, or HK$13,576 to HK$16,257 per square foot.

The discounted average price of the 368 units is HK$14,604 per square foot.

The project attracted many young homebuyers and investors.

13:00

How Hong Kong’s housing market became among the world’s most unaffordable

How Hong Kong’s housing market became among the world’s most unaffordable

“Long-term investors accounted for 20 per cent, a significant increase compared with before the withdrawal of purchasing curbs,” said Sandia Lau, Centaline Property’s Kowloon District director.

“This is all thanks to the significant reduction in home ownership costs, which attracts people to buy more than one house to collect rent, and the return is expected to be as high as 3 per cent.”

Late last month, Financial Secretary Paul Chan Mo-po scrapped all cooling measures restricting property transactions as he unveiled a budget aimed at restoring the city’s flagging fiscal health, addressing mounting calls from the property and business sectors to ditch the decade-old measures.

The scrapped measures include the Buyer’s Stamp Duty that targeted non-permanent residents and a New Residential Stamp Duty for second-time purchasers. Homeowners will also no longer need to pay a Special Stamp Duty if they sell their homes within two years.

The Hong Kong Mortgage Authority followed suit with its own easing measures. Homes valued at less than HK$30 million are now eligible for 70 per cent mortgage financing, compared with the previous cap of 60 per cent for flats valued between HK$15 million and HK$30 million.

The city’s property market could get an additional boost from a reduction in interest rates later this year.

The market expected lending rates to fall by 0.75 per cent, according to Sammy Po Siu-ming, CEO of Midland Realty’s residential division for Hong Kong and Macau.

He added that transactions on the first-hand market are expected to reach 4,500 this month, the highest since November 1998.

Source link