Bài viết này có khoảng 4203 từ, đọc toàn bộ bài viết mất khoảng 7 phút

Original: Odaily Planet Daily (@OdailyChina)

Author: Azuma (@azuma_eth)

The “de-pegging” situation of Strategy’s preferred stock STRC is worsening.

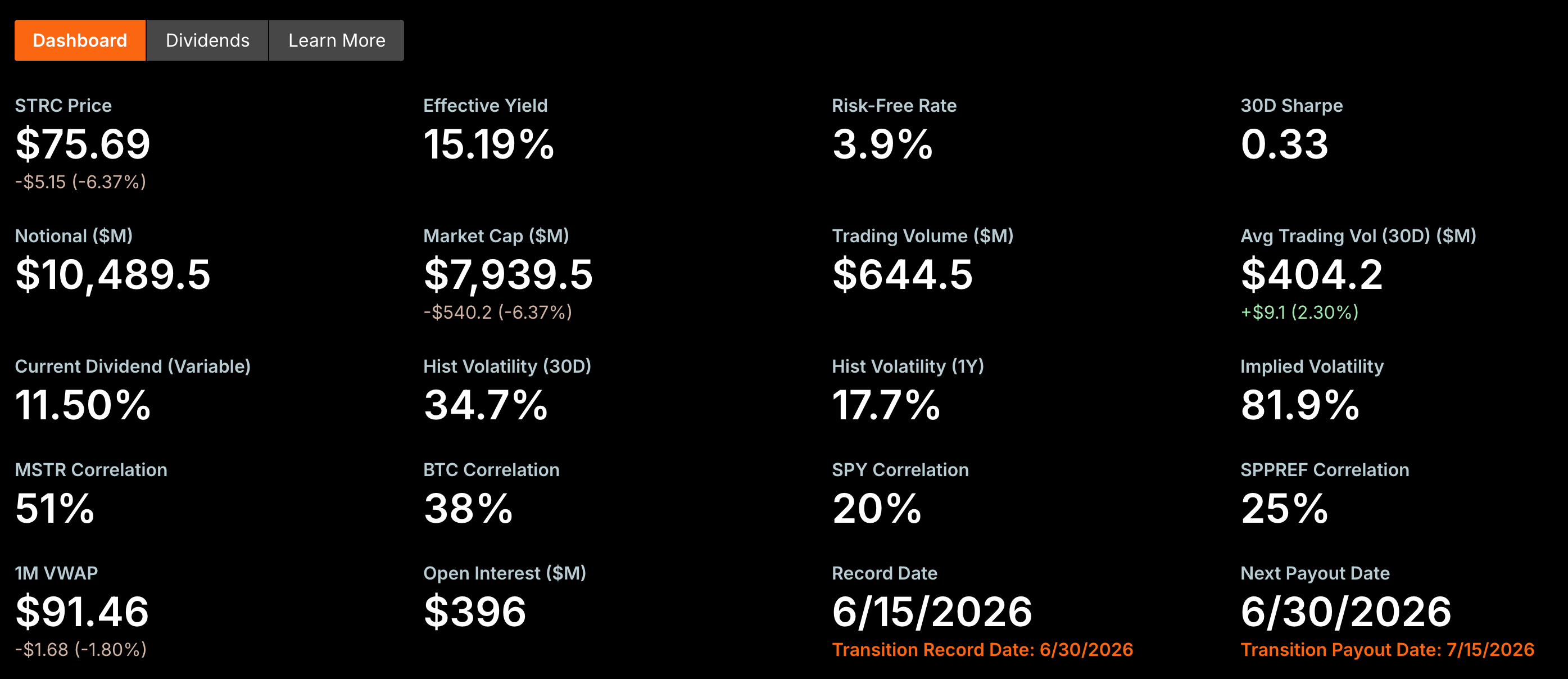

During U.S. stock trading hours yesterday, STRC fell below the 80 mark for the first time, hitting a low of $73.62. Although it rebounded slightly at the close, the price was still only $75.69, nearly 25% de-pegged from its target par value of $100.

Last week, we published an article on STRC’s de-pegging situation, titled “STRC De-pegs 11%, Can Strategy’s Perpetual Motion Machine Keep Running?“, focusing on the reasons for the de-pegging and briefly outlining the potential future impacts.

However, based on community discussions, it seems many readers still do not fully grasp the severe consequences of STRC’s persistent de-pegging, hence this follow-up article to dissect the issue.

Strategy’s Most Important Funding Channel Has Failed

What exactly is STRC? In a nutshell, it is Strategy’s cheapest and most efficient funding channel.

The essence of Strategy’s business model is continuously raising funds from the market to acquire more BTC, then raising more funds to buy more BTC. This is a cycle that must keep running. Strategy’s high valuation largely stems from the market’s belief in its ability to continuously raise funds and buy BTC. As long as this fundraising capacity exists, it can keep expanding its BTC holdings; conversely, the ever-increasing BTC holdings further support market expectations for its future fundraising ability.

Over the past few years, Strategy has tried almost every financing method – issuing common stock, convertible bonds, and various types of preferred stock – channeling the proceeds into BTC. Among all these tools, STRC was once considered by the market to be the closest to “perfect” and was also Michael Saylor’s proudest creation. Saylor once boasted, “STRC was designed by AI; humans couldn’t have designed it.”

As a preferred stock, STRC has clear advantages. Issuing common stock dilutes existing shareholders; issuing convertible bonds creates future debt repayment obligations. However, STRC, as a perpetual preferred stock, has no maturity date and doesn’t dilute common shareholders, only requiring the payment of a fixed dividend. For Strategy and Saylor, this is arguably the lowest cost and most efficient financing method.

At its inception, STRC was designed as a product pegged to $100. Strategy’s vision was to dynamically adjust the dividend rate to keep STRC trading around $100 (reminiscent of algorithmic stablecoins, isn’t it?). As long as the secondary market could maintain this price, the company could continuously issue new STRC near par value, constantly raising new funds to buy more Bitcoin.

In other words, STRC’s core value lies in its endless fundraising capability, but this capability is predicated on its price remaining near the target par value. When STRC persistently de-pegs, this funding channel is effectively blocked. After all, if an investor can buy the same STRC on the secondary market for just $75, there is no incentive to participate in a new company issuance at nearly $100.

For Strategy, options are either to keep raising the dividend rate to attract capital (which has proven to be of limited appeal) or to accept the reduced efficiency of discounted issuance (which effectively breaks the original target par value). Either way, friction within this fundraising machine is growing significantly.

From Financing Tool to Cash Flow Burden

If it were just a temporary loss of fundraising capability, it might be manageable. The bigger problem is that STRC requires Strategy to continuously pay substantial cash dividends.

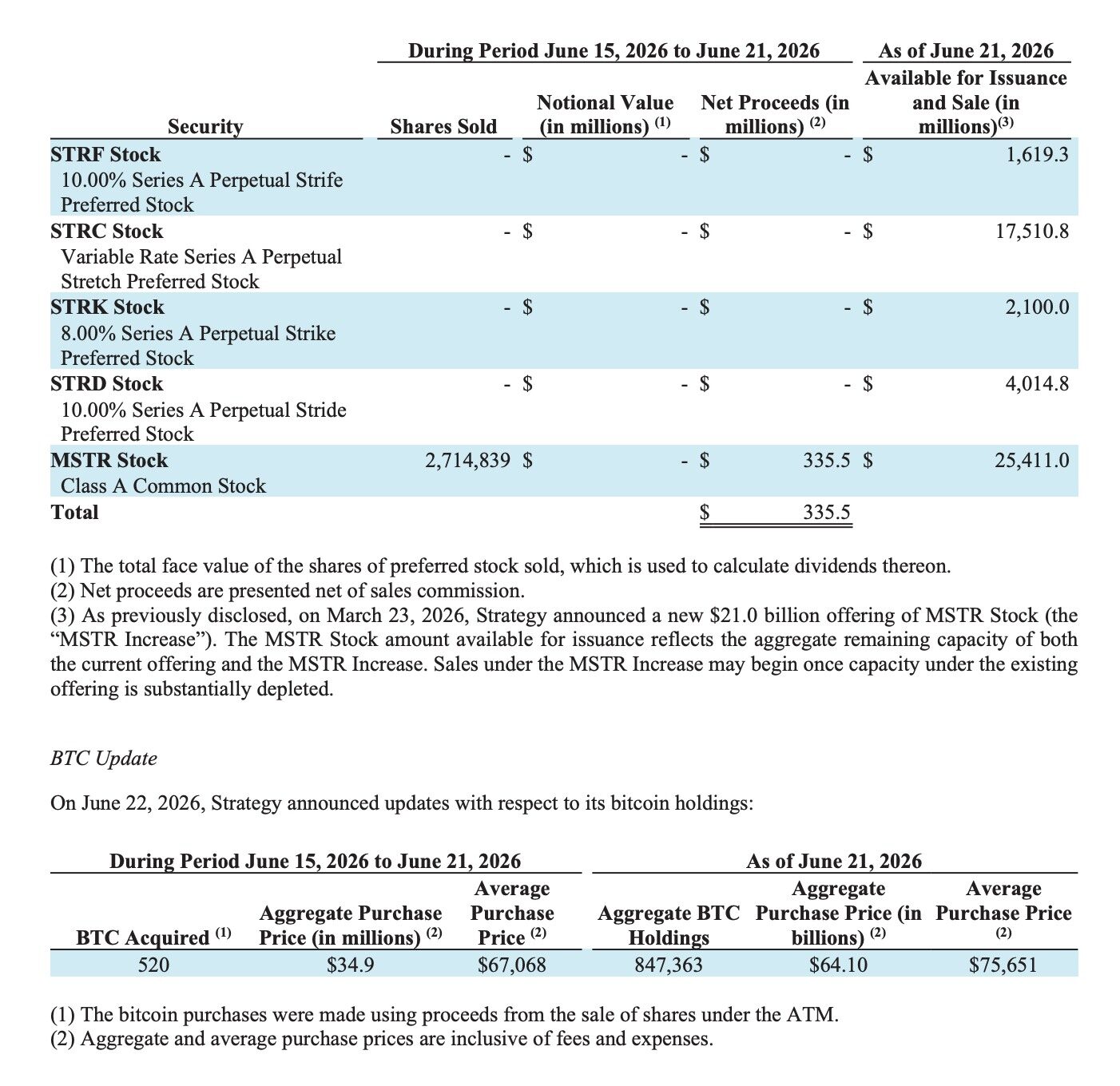

According to the latest official data from Strategy, the total issuance size of STRC has reached approximately $10.49 billion, with a current dividend yield of 11.5%. This means that STRC alone entails an annual cash dividend payment obligation exceeding $1.2 billion. When adding Strategy’s other preferred stocks like STRD, STRK, and STRF, this figure climbs to around $1.7 billion annually.

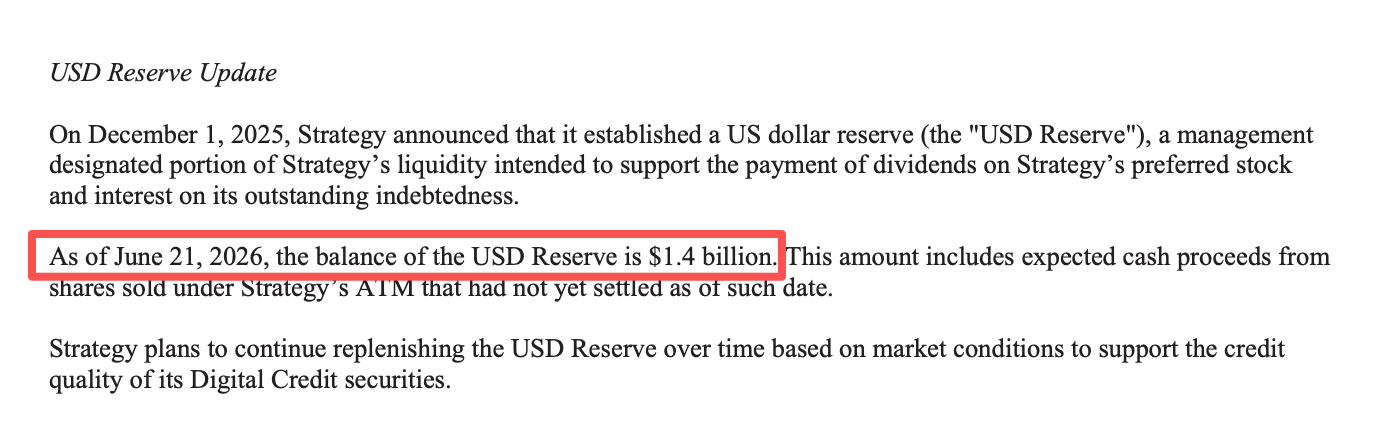

In a common stock offering filing dated June 21 (note: common stock, detailed below), Strategy disclosed its cash reserves stood at approximately $1.4 billion. At this level of cash reserves, Strategy’s book cash can cover less than one year of preferred stock dividend payments.

Breaking the Deadlock Requires Money, But Where Will It Come From?

Whether to sustain its business model or escape its dire cash flow situation and avoid dividend payment defaults (the more pressing issue), Strategy needs more capital. Theoretically, only three viable paths for “raising money” remain available.

First, Issuing Common Stock.

This is currently the most direct and mature fundraising method. Through its At-the-Market (ATM) offering program, Strategy can continuously sell MSTR common stock to raise funds.

However, common stock financing is not without cost. Continuous issuance increases the number of outstanding shares. If the BTC bought with the new capital cannot outpace the rate of share dilution, the BTC Per Share growth will slow, and common shareholders will face persistent dilution. Note this carefully – the following is crucial.

Second, Continue Issuing Debt.

Over the past few years, Strategy has frequently raised funds through debt instruments like convertible bonds. This was a significant source of capital for its early large-scale BTC acquisitions.

However, as its preferred stock scale expands and fixed cash dividend payments rise, the market is paying closer attention to Strategy’s liquidity and debt repayment capacity. In the current financing environment, if the company issues bonds again, investors will likely demand a higher risk premium, meaning financing costs would be significantly higher than in the past.

More importantly, unlike preferred or common stock, bonds carry rigid interest and principal repayment obligations. Against the backdrop of declining cash reserves and rising dividend expenses, further increasing debt levels will undoubtedly exacerbate the company’s financial burden and compress future financing flexibility.

Third, Selling BTC.

From a financial standpoint, this is the fastest way to replenish cash reserves. Strategy has certainly considered this path. Its official X account once posted regarding the dividend payment pressure, stating: “If its massive Bitcoin reserve is considered, it’s enough to cover 32 years of dividend payments.”

For Strategy, however, this is an extremely risky choice. Earlier this month, Strategy sold a portion of its Bitcoin holdings for the first time. Although the sale was small (32 BTC) and was framed by the company as a “proactive market desensitization test” with mention of buying back more later, the move still caused a sharp short-term market decline.

As the largest single Bitcoin holder in the world, Strategy’s actions can easily trigger market chain reactions. If it increases the sale volume in the future, it would undoubtedly have a massive impact on an already fragile BTC price. If BTC declines further, Strategy’s so-called “reserve” would also shrink rapidly.

In summary, under the current circumstances, every feasible financing channel available to Strategy comes at a higher cost than in the past.

Has Strategy Made Its Choice?

Looking at Strategy’s latest moves, besides hinting at potentially selling BTC, the company appears to have chosen its path.

Since June, Strategy has conducted three consecutive weekly fundraising rounds via its common stock ATM program. The most recent round (June 22) is particularly telling.

According to the latest 8-K filing by Strategy, the company sold 2,714,839 shares of MSTR common stock within a week, raising a total of $335.5 million. However, during that same week, Strategy only purchased 520 BTC, spending a total of $34.9 million at an average price of approximately $67,068. In other words, of the $335.5 million raised, only about 10% was actually used to increase BTC holdings, while the rest was primarily used to replenish the company’s cash reserves, increasing its cash position from roughly $1.1 billion to the current roughly $1.4 billion.

Seems effective, doesn’t it? But there’s another catch here.

For MSTR common shareholders, the most critical metric to watch is: How much BTC can the funds raised from each newly issued common share ultimately buy, and is it enough to cover the BTC equity that share represents? If the new financing buys more BTC than the share originally represented, then the common shareholder’s equity is actually enhanced. Conversely, if the funds are insufficient to cover the BTC equity corresponding to the new share, then common shareholders suffer dilution.

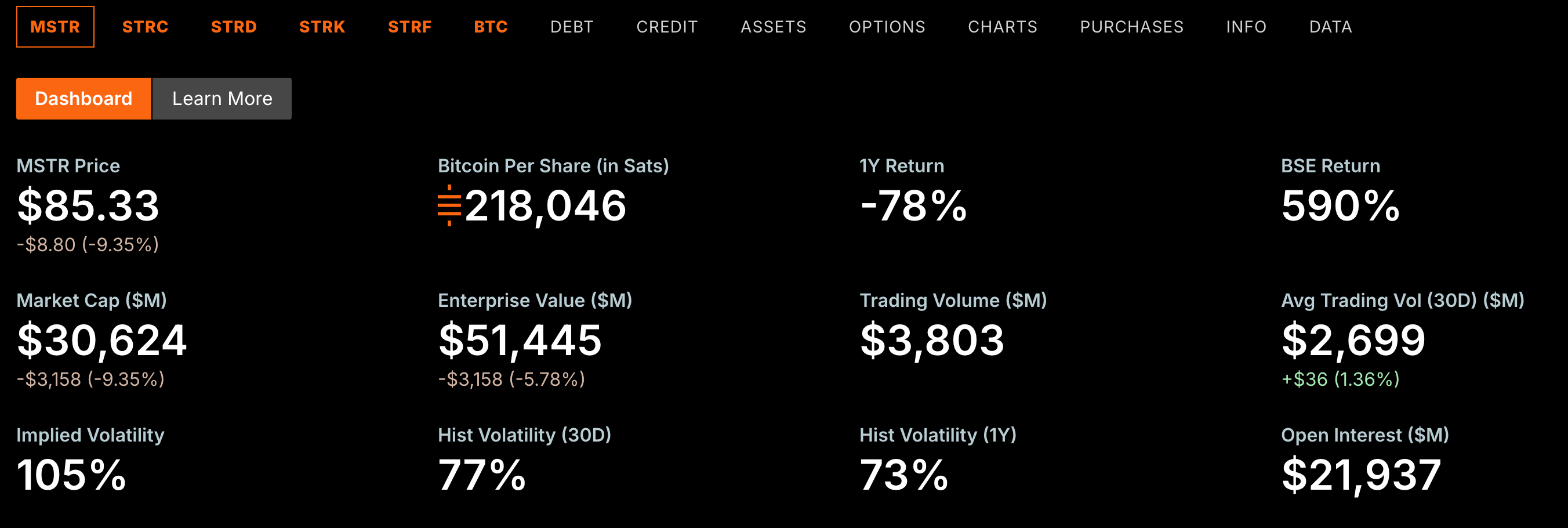

Clearly, Strategy’s recent common stock issuances have come at the expense of diluting common equity. Official Strategy data also shows that MSTR’s BTC Per Share has decreased from a peak of 220,900 Sats to 218,046 Sats.

This highlights the fundamental limitation of common stock financing. For most listed companies, issuing additional common stock is just one of many financing options. But for Strategy, the common stock itself is integral to its business model.

Over the past few years, Strategy’s ability to grow continuously has been based on the perpetual motion of this flywheel: “Raise funds ➡️ Buy coins ➡️ Solidify market expectations ➡️ Raise more funds ➡️ Buy more coins…” The core market expectation for Strategy is that it can continuously create more BTC equity for common shareholders, not dilute it.

However, when Strategy is increasingly forced to rely on common stock issuance to replenish cash reserves rather than continue accumulating BTC, the flywheel’s logic changes. While common stock financing can temporarily alleviate Strategy’s cash pressure, it is difficult to become a long-term replacement for STRC.

Once common stock issuance persistently erodes the BTC equity per share, the very foundation upon which MSTR’s high premium depends could be challenged, and this is precisely the core competitive advantage of the entire Strategy business model.

What Happens to BTC?

Over the past few years, Strategy has become the most significant marginal buyer in the BTC market (arguably without equal). To date, Strategy holds a total of 847,363 BTC, representing about 4% of the current circulating supply, valued at over $50.7 billion. The market has long been accustomed to Saylor’s massive, regular weekly purchases.

But that is changing. While Strategy can still raise funds through common stock, most of the capital is no longer flowing into BTC, but is prioritized for replenishing cash reserves. This means that, given the same fundraising scale, the net new buying pressure entering the BTC market is diminishing.

More concerning is that this situation is likely to persist. If STRC cannot regain its peg for an extended period, its preferred stock funding channel remains blocked, forcing Strategy to rely on common stock issuance for cash flow for a long time, potentially further reducing the proportion of funds used for BTC accumulation. For the BTC market, this means the most stable and certain institutional buying force of the past will no longer grow continuously as it did before.

But what warrants more caution is this: if common stock issuance overly dilutes MSTR shareholder equity, Strategy might be forced to consider another funding channel – selling coins.

From diminishing new buy-side pressure to the potential emergence of sell-side pressure, Strategy today is no longer just the largest marginal buyer of BTC; it has become a giant sword hanging over BTC.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment