Pound Sterling will start the new week with the wind at its back against the US Dollar, but the next move depends less on UK politics and more on whether last week’s US jobs disappointment turns into a broader rethink of Federal Reserve policy.

The US Dollar suffered its biggest weekly drop since April after June payrolls slowed and earlier months were revised lower, leaving traders less convinced that another near-term Fed rate increase is imminent.

Pound Sterling also benefited from easing domestic political risk, with the GBP/USD exchange rate ending last week close to 1.3350.

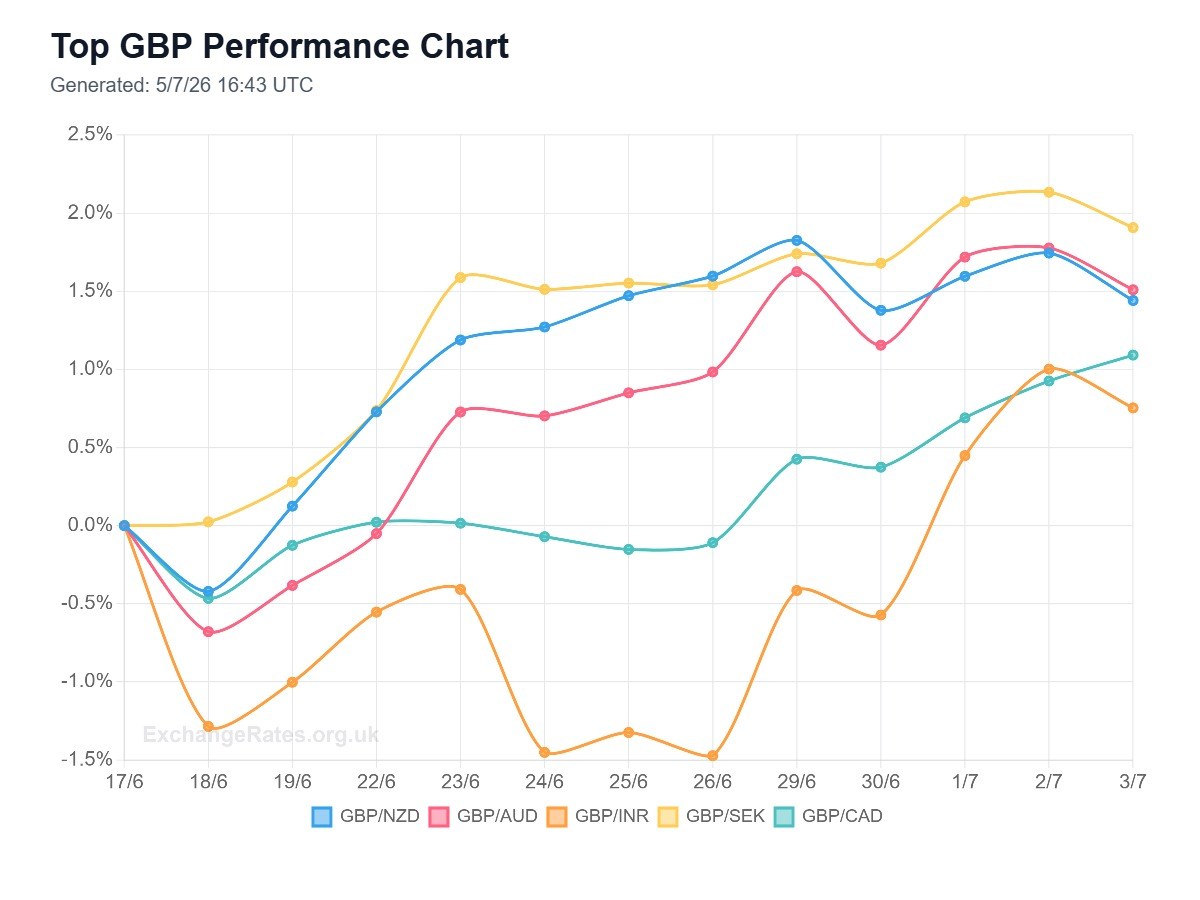

The latest GBP snapshot shows Sterling’s best one-day gains against the Canadian Dollar, Hong Kong Dollar, US Dollar and Chinese Yuan, while the New Zealand Dollar, Australian Dollar, Indian Rupee and Swedish Krona were the strongest performers against the Pound.

Positioning is therefore cleaner than it was earlier in June: investors are still prepared to buy Sterling on dips, but the strongest GBP crosses are vulnerable to profit-taking if global risk appetite improves.

This week’s calendar gives markets plenty of reasons to reassess that positioning.

US ISM Services opens the week, the Bank of England publishes its Financial Stability Report on Tuesday, FOMC minutes arrive on Wednesday, China inflation is due Thursday and Canadian labour-market data closes the week on Friday.

Oil-sensitive currencies will also react to the latest OPEC+ decision to raise August output targets by 188,000 barrels per day, a move that has kept crude prices under pressure as the Strait of Hormuz gradually reopens.

GBP/USD – 1.335103 (+0.09%)

The Pound to Dollar exchange rate enters the week near recent highs after softer US employment data forced investors to trim Federal Reserve tightening bets.

Futures now imply a much lower probability of a July hike, while the September pricing has also been cut back, giving Sterling room to hold above the 1.33 area.

The risk is that Monday’s ISM Services data or Wednesday’s FOMC minutes push back against the dovish interpretation of payrolls.

A sustained move above 1.3380 would put 1.34 back in play, while a hawkish Fed tone would expose 1.3280.

Pound Sterling Prices: This Week

| USD | EUR | GBP | JPY | CAD | AUD | NZD | CHF | |

|---|---|---|---|---|---|---|---|---|

| USD | -0.43% | -1.15% | -0.24% | +0.04% | -0.63% | -1.30% | -0.80% | |

| EUR | +0.43% | -0.72% | +0.19% | +0.47% | -0.20% | -0.87% | -0.37% | |

| GBP | +1.16% | +0.72% | +0.92% | +1.20% | +0.52% | -0.15% | +0.35% | |

| JPY | +0.24% | -0.19% | -0.91% | +0.28% | -0.39% | -1.06% | -0.56% | |

| CAD | -0.04% | -0.47% | -1.19% | -0.28% | -0.67% | -1.34% | -0.84% | |

| AUD | +0.64% | +0.20% | -0.52% | +0.39% | +0.68% | -0.67% | -0.16% | |

| NZD | +1.32% | +0.88% | +0.15% | +1.07% | +1.36% | +0.68% | +0.51% | |

| CHF | +0.80% | +0.37% | -0.35% | +0.56% | +0.84% | +0.17% | -0.51% |

The FX heat map compares how Pound Sterling (GBP) has performed against a basket of major currencies over the past week. The largest move was against the Canadian Dollar, where Pound Sterling made its strongest advance. Data comparing prices today (05/07/2026 17:19 UTC) and daily close on 28/06/2026.

To read the table, choose the base currency from the left-hand column and then move across to the quote currency along the top row. For example, the GBP row and USD column shows the weekly percentage move in GBP/USD.

GBP/EUR – 1.167445 (-0.02%)

GBP/EUR remains close to 2026 highs, but the pair has lost some momentum as Euro buyers return after the Dollar’s pullback. The Eurozone inflation backdrop is less urgent than it was a few weeks ago, with June inflation slowing to 2.8% from 3.2%, reducing pressure for an immediate ECB follow-up hike. That leaves the cross driven by relative policy patience: Bailey has pushed back against rate-cut talk, while the ECB accounts on Thursday will show how divided policymakers are after June’s move. A break of 1.17 would be technically important.

GBP/JPY – 215.428111 (+0.03%)

Pound Sterling remains elevated against the Yen as rate differentials continue to favour the Pound, but intervention risk is now a clear ceiling for GBP/JPY. Japan’s authorities have kept the threat of currency action alive after the Yen rebounded from 40-year lows, and thin summer liquidity could make traders more cautious about chasing the pair above 216. This week’s Japanese household spending and wage data will matter because stronger pay growth would support the case for gradual Bank of Japan tightening. Until that changes, Sterling dips are likely to find demand.

GBP/AUD – 1.923707 (-0.26%)

GBP/AUD begins the week softer as the Australian Dollar benefits from better global risk sentiment and a weaker US Dollar. The pair remains high by recent standards, but positioning is now vulnerable after Sterling’s strong June advance. Australia’s TD-MI inflation gauge on Monday, building approvals on Wednesday and RBA commentary will be watched for signs that inflation pressure remains sticky. The Reserve Bank of Australia held rates at 4.35% in June and warned hikes may not be over, which gives the Aussie some protection if local data surprise higher.

GBP/CAD – 1.895902 (+0.16%)

GBP/CAD is one of Sterling’s strongest crosses and is trading close to fresh year-to-date highs. The Canadian Dollar has been unable to fully benefit from the softer US Dollar because oil prices remain under pressure after OPEC+ agreed another output increase from August. That matters for CAD because energy prices feed directly into Canada’s terms of trade. The week’s domestic calendar is heavy, with Canadian PMI data and Bank of Canada surveys on Monday, trade figures on Tuesday and June employment data on Friday. A soft jobs print would keep GBP/CAD supported above 1.89.

GBP/CHF – 1.072704 (-0.03%)

GBP/CHF remains rangebound as two opposing forces offset each other. Firmer global equity markets reduce defensive demand for the Swiss Franc, but geopolitical risk and unease around intervention-sensitive currencies keep some safe-haven demand alive. Sterling’s yield advantage remains helpful, especially after Bailey signalled that UK rate cuts are not back on the table. The cross needs a cleaner risk-on move to challenge the 1.0760 area; otherwise, investors may keep fading rallies while waiting for US services data and the FOMC minutes to set the broader risk tone.

GBP/NZD – 2.336614 (-0.30%)

The New Zealand Dollar was the strongest major currency against Sterling in the latest snapshot, helped by the same risk-positive backdrop supporting other high-beta FX. GBP/NZD is still historically elevated after Sterling’s strong run, so the early-week bias is toward consolidation unless global risk appetite turns lower. With few major New Zealand releases on the attached calendar, the Kiwi will take much of its direction from China inflation on Thursday, global equities and US rate expectations. A softer FOMC message would favour NZD, while renewed risk aversion would quickly restore Sterling demand.

GBP/CNY – 9.064013 (+0.09%)

GBP/CNY starts the week above 9.06, with Pound Sterling still supported by UK rate expectations but the Yuan cushioned by broad Dollar weakness. China’s inflation data on Thursday is the key event for this cross. Producer prices had already risen to their highest level in almost four years in May as energy costs fed into factory-gate inflation, so another firm PPI reading would complicate the PBOC’s ability to provide more support to growth. Weak CPI, however, would keep concerns over domestic demand alive and leave GBP/CNY biased higher.

GBP/SEK – 12.894777 (-0.22%)

GBP/SEK has eased from recent highs as the Swedish Krona benefits from improved European risk sentiment and a softer Dollar. The pair remains elevated after Sterling’s strong June performance, but the Riksbank backdrop is no longer straightforwardly negative for SEK. Sweden’s central bank is expected to stay cautious, though economists have seen a rising chance of another hike later this year if inflation pressure persists. Eurozone retail sales, German production and the ECB accounts will also matter because SEK tends to track broader European growth expectations.

GBP/NOK – 13.145449 (-0.02%)

GBP/NOK is little changed, but the Norwegian Krone remains hostage to oil. Sterling’s strong June rally against NOK has left the cross vulnerable to profit-taking, yet lower crude prices continue to limit Krone demand. The OPEC+ decision to raise August production targets adds another supply-side headwind for oil-linked FX, while Friday’s IEA Oil Market Report could reinforce or challenge that move. If crude remains heavy, GBP/NOK should stay supported above 13.10; a sharp oil rebound would be the clearest risk to Sterling longs.

GBP/SGD – 1.724552 (+0.01%)

GBP/SGD is stable as the Singapore Dollar tracks the broader Asian FX response to a weaker US Dollar. Sterling still has the yield advantage, but SGD tends to perform better when global risk appetite improves and US rate expectations fall. Singapore retail sales on Monday and foreign exchange reserves on Tuesday are unlikely to dominate the cross unless they surprise sharply. China inflation on Thursday and the FOMC minutes on Wednesday should matter more for direction. A break above 1.7270 would keep Sterling’s July uptrend intact.

GBP/MXN – 23.323445 (+0.04%)

GBP/MXN is broadly steady, with the Peso still supported by carry demand but less insulated than usual after softer Mexican inflation reduced pressure on Banxico to tighten policy. Mexico’s June inflation data and monetary policy minutes arrive on Thursday, followed by industrial production on Friday, giving traders a fresh read on whether domestic rate support remains strong enough to offset global volatility. Softer US yields normally help MXN, but any rebound in Dollar demand after the FOMC minutes would leave GBP/MXN vulnerable to a renewed move higher.

GBP/ZAR – 21.670405 (-0.13%)

GBP/ZAR has slipped as the Rand benefits from weaker US yields, softer oil prices and better global risk appetite. The move is still fragile because South Africa’s domestic data remain mixed; manufacturing sentiment weakened in June and Thursday’s manufacturing production figures will test whether that softness is spreading. For now, the Rand is trading more like a global risk proxy than a local-data story. If US data keep the Dollar under pressure, GBP/ZAR could drift lower, but any deterioration in risk sentiment would quickly restore Sterling’s defensive appeal.

Week Ahead: Key Events – July 6-10, 2026

- Monday: UK S&P Global Construction PMI, Eurozone retail sales and PPI, US ISM Services PMI, Bank of Canada Business Outlook Survey, Bank of Canada consumer expectations survey, Fed Waller speech, ECB Schnabel, Lagarde and Lane speeches.

- Tuesday: Japan household spending and cash earnings, German industrial production, UK Halifax house prices, UK BBA mortgage rate, Bank of England Financial Stability Report, Canada and US trade balances, Canada Ivey PMI, US consumer inflation expectations.

- Wednesday: RBA Hunter speech, Australian building permits, UK gilt tenders, US wholesale inventories, EIA oil inventories, US 10-year note auction and FOMC minutes.

- Thursday: UK RICS house price balance, China CPI and PPI, German trade balance, ECB Monetary Policy Meeting Accounts, US initial jobless claims, US existing home sales, Fed Williams and Fed Logan speeches, Mexico inflation and Banxico minutes.

- Friday: Japan PPI, German and French final inflation, Italian industrial production, IEA Oil Market Report, India credit and FX reserves data, Canadian employment report and building permits, US WASDE and Baker Hughes rig count.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment