Precious metals remain in an intermediate correction, but several real-money sentiment indicators suggest the market is working its way into the later innings of this pullback. While technical charts still point to potential downside, sentiment data indicates any lower lows would likely be unsustainable .

Institutional Positioning Shows Limited Enthusiasm

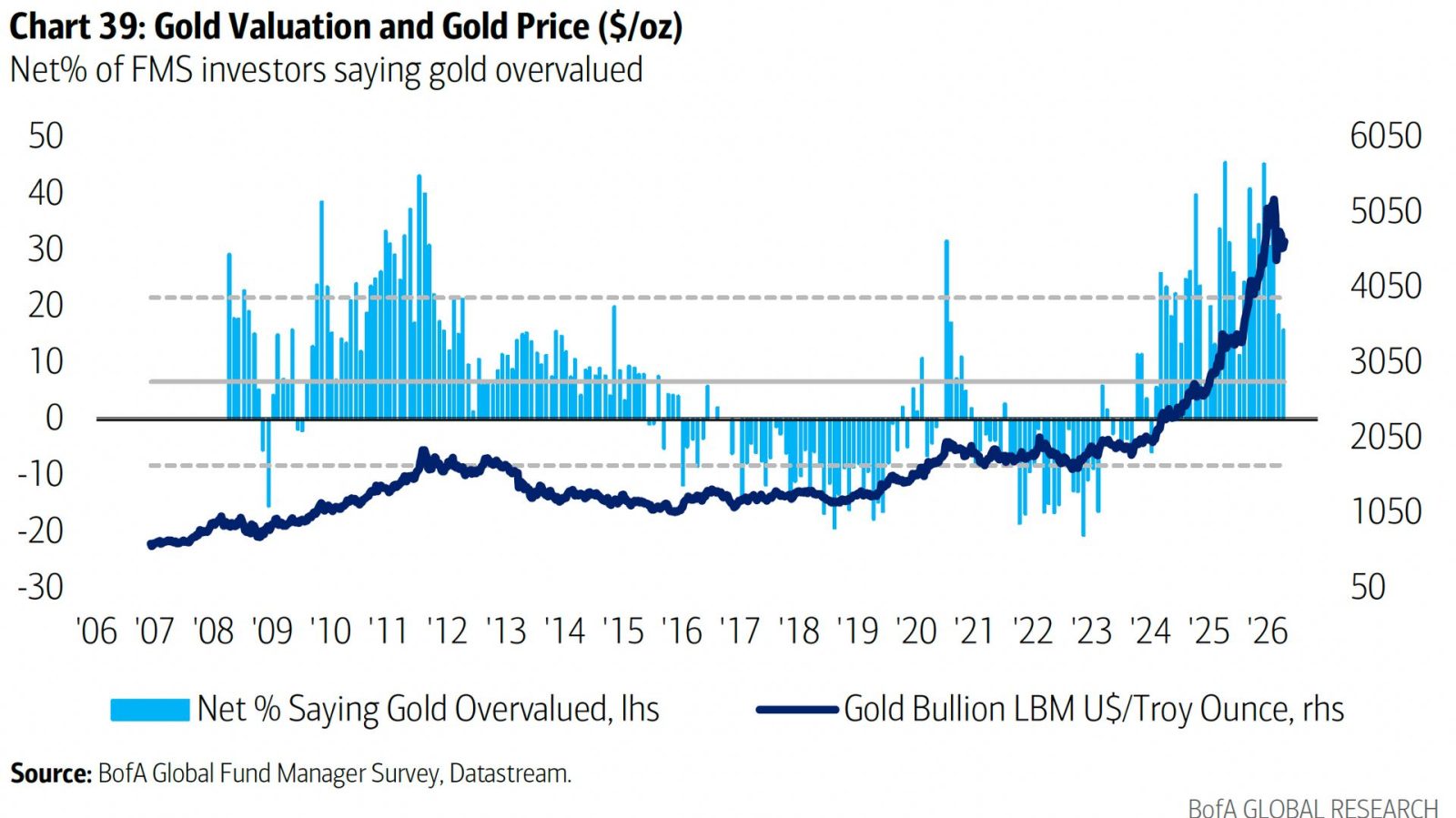

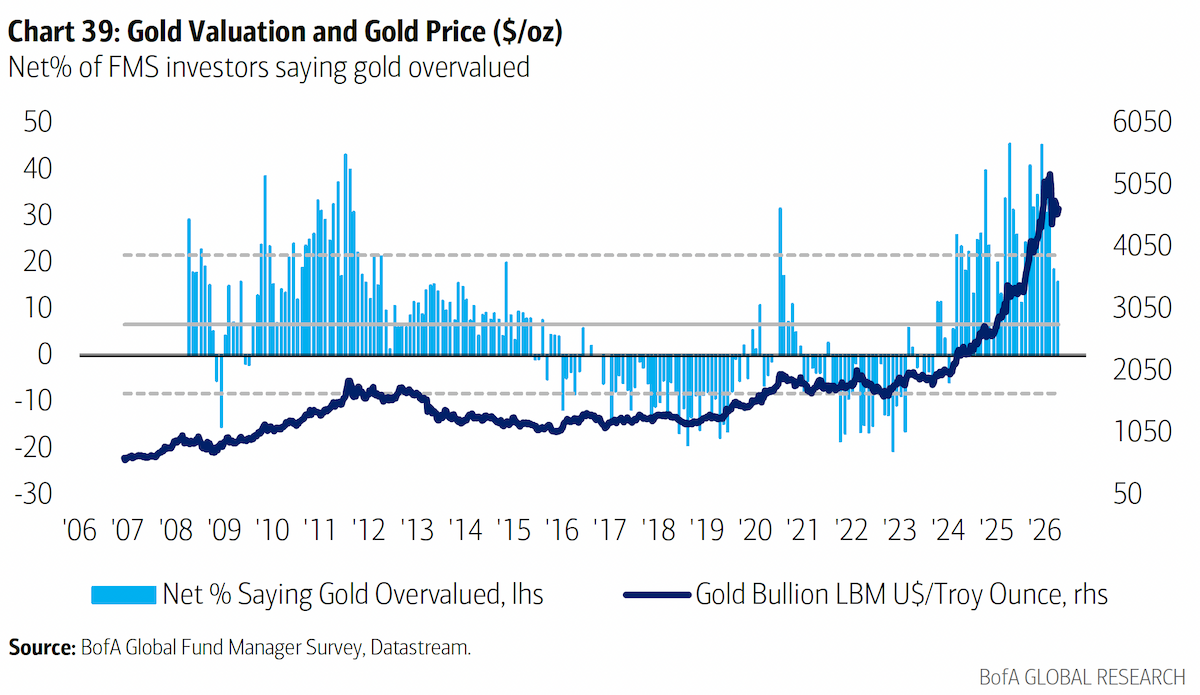

The Bank of America Global Fund Manager Survey reveals that a net 16% of managers currently consider gold overvalued . This marks the lowest reading in the past 10 months and the second-lowest in 15 months, indicating professional investors have turned increasingly skeptical during this correction .

More striking is the data from family offices: according to the JPMorgan 2026 Global Family Office Report covering 333 single family offices from 30 countries with average net worth of $1.6 billion, 72% own no gold whatsoever. Among the 28% who do hold gold, the average allocation stands at just 0.9%.

ETF Holdings Reveal Stark Underinvestment

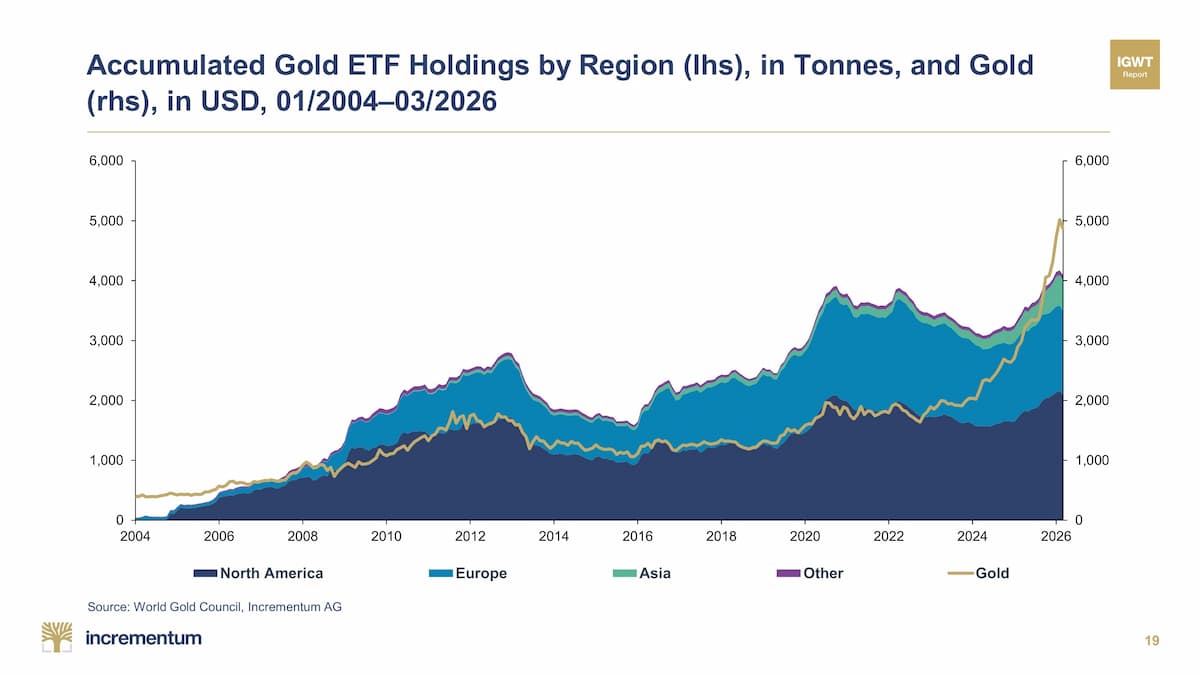

Despite gold trading roughly 100% higher than its 2020 peak, gold ETF holdings (as of March) are only slightly above their 2020 levels and may be even lower today. This disconnect between price appreciation and investor positioning highlights the absence of speculative excess that typically marks significant market tops.

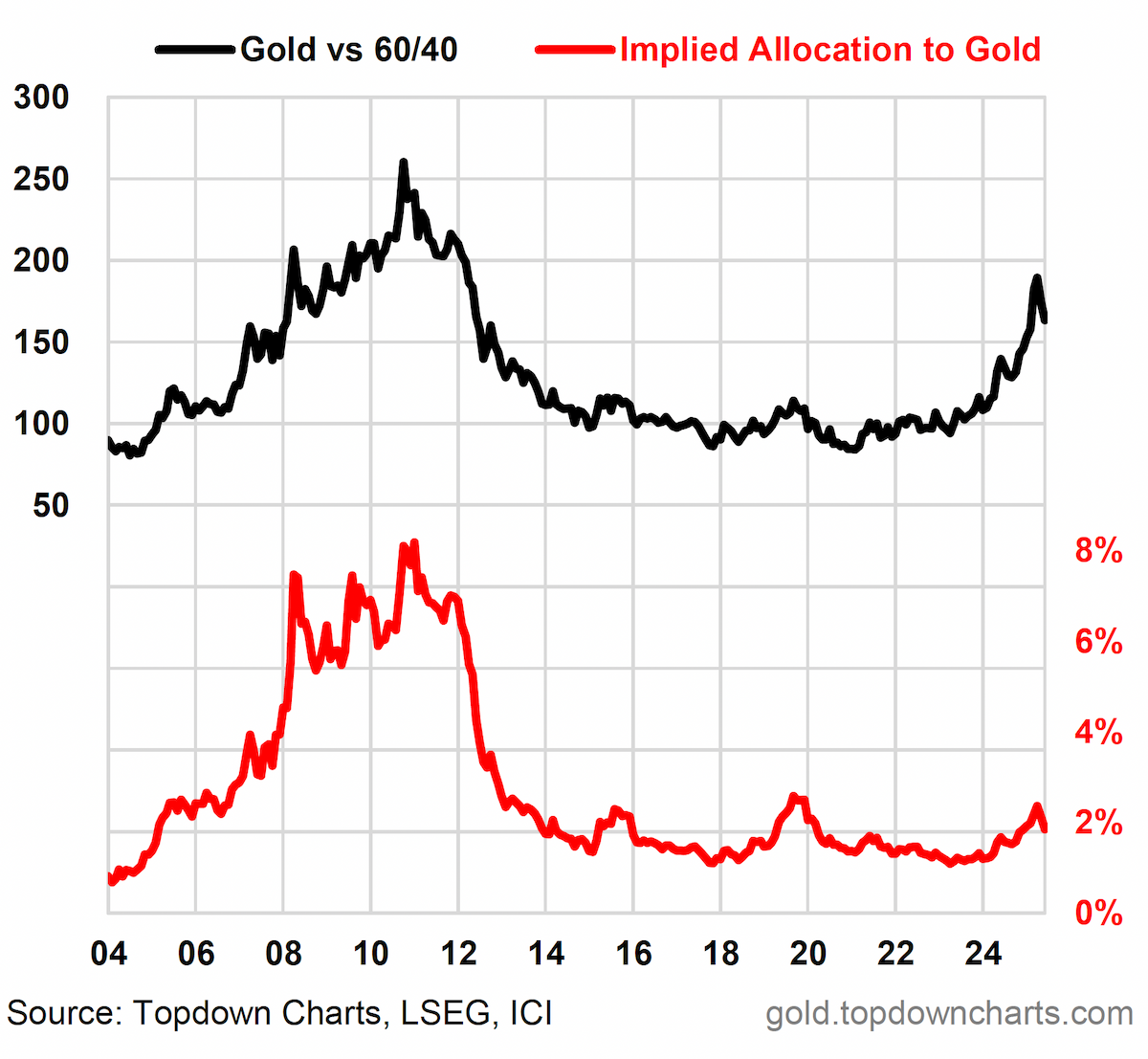

Gold ETFs currently comprise less than 2% of total ETF assets. This allocation sits below the 2019 peak and far below the 2011 peak when gold ETFs represented over 8% of total ETF assets. The data suggests that while gold has declined against the traditional 60/40 portfolio and equities, investor allocation has not followed price performance.

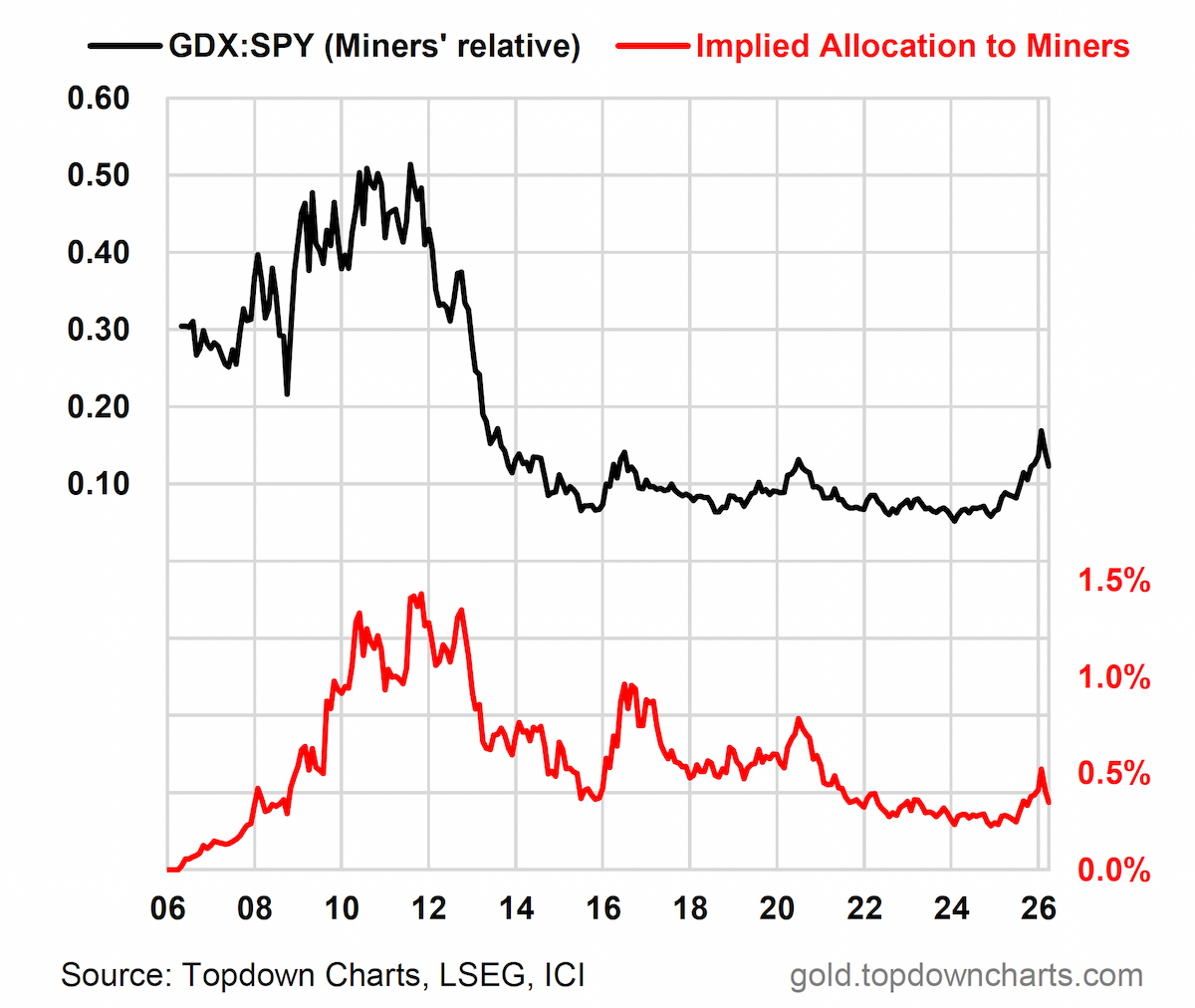

Gold Mining Stocks Show Even Greater Underallocation

Gold miner ETFs tell an even more extreme story. Miner ETFs now comprise approximately 0.37% of ETF capital, down from roughly 0.52% a few months ago. This represents levels below both the 2020 and 2016 peaks.

The Bull Market Backdrop

The sentiment picture strongly supports the thesis that gold and gold stocks remain in the early innings of a secular bull market, with the current cyclical bull that began about 2.5 years ago not yet halfway complete. A substantial portion of capital remains parked in conventional equities, creating potential fuel for future precious metals rallies .

Historically, cyclical peaks in gold are preceded by a flush of capital out of stocks and into precious metals—a dynamic clearly absent from current positioning data. While this correction has successfully reset sentiment and technical indicators may suggest additional near-term downside, the fundamental lack of speculative positioning argues against a sustained breakdown from here.

Disclaimer: The views expressed in this article are those of the author and may not reflect those of Kitco Metals Inc. The author has made every effort to ensure accuracy of information provided; however, neither Kitco Metals Inc. nor the author can guarantee such accuracy. This article is strictly for informational purposes only. It is not a solicitation to make any exchange in commodities, securities or other financial instruments. Kitco Metals Inc. and the author of this article do not accept culpability for losses and/ or damages arising from the use of this publication.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment