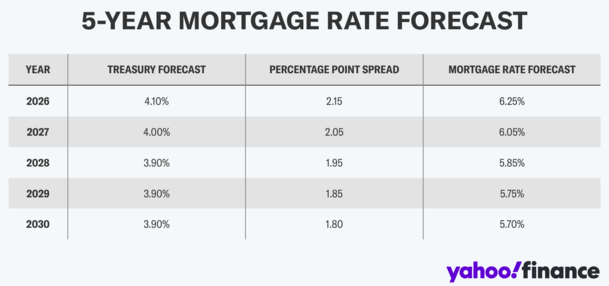

The brains over at Yahoo Finance set out to determine a five-year mortgage rate forecast using traditional research and Anthropic’s Claude.

When combining 10-year treasury yield forecasts with projected spreads, they came up with 30-year fixed mortgage rates for the next five years.

What they discovered is that mortgage rates are largely expected to go down, from around 6.25% this year to 5.70% by the year 2030.

In other words, the rate you see today might be the highest rate you’ll see for a long time, barring the typical, short-term ebb and flow.

Which begs the question, if rates are going to be lower, why go with a 30-year fixed?

Are We Overly Reliant on the 30-Year Fixed Mortgage?

I feel like we’re too reliant on the 30-year fixed mortgage.

Beyond that, often times it just becomes the default loan option without further consideration.

It seems nobody even talks about alternatives, be it the 5/1 ARM or the 7/6 ARM.

Those products are out there, but often only account for a tiny slice of the overall mortgage market.

And often they just go to wealthy folks who are more savvy and capable of handling any downside that might come with an adjustable-rate mortgage.

Now don’t get me wrong. The 30-year fixed is incredible. It’s uniquely American and one of the best tools a homeowner has at their disposal.

But mortgage rates aren’t on sale anymore. Locking in a super low rate isn’t a possibility in 2026.

Those days are long gone. Today, the 30-year fixed is more or less close to its long-run average.

It’s actually a little bit below if we go all the way back to the early 1970s, as it averaged roughly 7.75% since then.

Mortgage Rates Are No Longer on Sale

The point is it’s not a screaming deal at the moment, so locking in that rate for the next 30 years might not be so valuable.

Especially if these rate forecasts from Yahoo Finance turn out to be correct.

Simply put, it made a whole world of sense to lock in a rate of 2-4% for the next 30 years. But a 6 or 7% rate? Ehh.

There might be a better alternative – an adjustable-rate mortgage, such as a 5- or 7-year ARM that’s fixed for the first 60 or 84 months respectively.

That means it’s a hybrid loan, with a fixed-rate period for quite a long time before you have to worry about the rate adjusting.

And even after that time, the rate may not even adjust higher.

If we take these estimates at face value, rates are projected to move lower between now and the year 2030.

That makes it less favorable to lock the rate in for the next three decades, since it’s not so special.

ARMs Can Offer a Substantial Discount If You Pick the Right Lender

So if you took out say a 5-year ARM today, it wouldn’t have its first adjustment until 2031.

If mortgage rates were to fall at any point along the way, you could do a rate and term refinance and take advantage of that.

This is also true if you opt for a 30-year fixed. You could refinance that into another fixed-rate loan if you wanted.

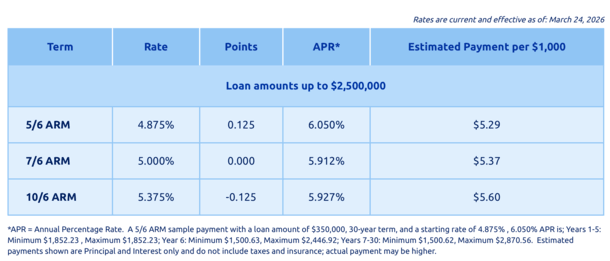

But with the ARM, you get a discount. And that discount can be sizable, perhaps even 1% lower than the 30-year fixed.

This lender above has a 30-year fixed at 6.375%, or a 7/6 ARM at 5%! Huge difference. And in the 4s for a 5/6 ARM.

That’s the whole point. If you lock in the 30-year fixed at 6.50% or whatever it happens to be, you’re betting on rates going higher.

If they don’t, you don’t get any upside. You pay for the safety of that rate not going higher, even if it never actually does.

With the ARM, you get the discount because those assurances aren’t baked into the loan.

So that’s the downside. That’s why most people don’t take out ARMs.

Anything Is Possible with Mortgage Rates

Anything is possible with mortgage rates. They could surge over the next five years, at which point the ARM would be a huge liability.

This happened to those who went with ARMs back in 2017-2021, and failed to refinance before rates shot higher.

But that was when rates were historically well below average (or at record lows). As noted, they are now pretty much in line with long-term averages.

The other issue is you might not be able to refinance. Imagine property values plummet and you’re upside down on the loan.

Of course, that too would go against history, as nominal home price declines are exceedingly rare.

There’s also the issue of qualifying for a mortgage, assuming you lose your job, have bad credit, etc.

So a mortgage refinance is never a slam dunk. Things can come up, and with the 30-year fixed you don’t have to worry about it.

But you do need to look at mortgage rates a little differently today because they’re back to normal.

As such, looking beyond just the 30-year fixed is something we should all consider.

Even if you can’t refinance once the adjustable-rate period ends, you might not need to. The fully-indexed rate could be just fine.

Not to mention all the savings during the first five or seven years.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 19 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on X for hot takes.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Leave a comment